- +1-315-215-1633

- sales@thebrainyinsights.com

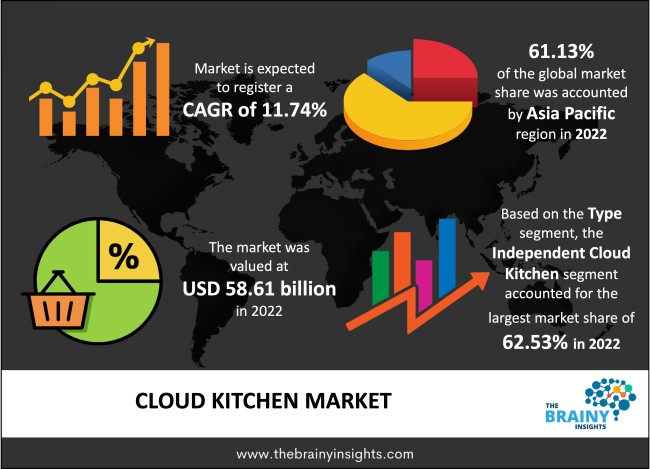

The global Cloud Kitchen market generated USD 58.61 billion revenue in 2022 and is projected to grow at a CAGR of 11.74% from 2023 to 2032. The market is expected to reach USD 177.85 billion by 2032. The increasing global population, growing disposable income, the desire for convenience, and the widespread adoption of digital technologies collectively propel the global cloud kitchen market. Furthermore, a substantial shift in consumer preferences towards online food delivery over traditional dine-in experiences has notably heightened the demand for cloud kitchen services. Additionally, social distancing measures and lockdowns led to an increased reliance on food delivery, prompting consumers and businesses to embrace the convenience of cloud kitchens.

A cloud kitchen, a virtual or ghost kitchen, is a culinary concept that operates solely for food preparation and delivery, bypassing the traditional dine-in experience. Unlike brick-and-mortar restaurants, cloud kitchens do not have a physical area like a storefront or dining area for customers. Instead, they leverage digital technology and online platforms to receive orders and fulfil deliveries or takeout. Cloud kitchens operate primarily through digital channels, leveraging online platforms, mobile applications, and third-party delivery services to connect with customers. Ordering, payment, and communication occur virtually. Sometimes, a single cloud kitchen may house multiple virtual restaurant brands, each specializing in specific cuisines or food categories. This factor allows for diversification and experimentation in menu offerings. Cloud kitchens employ data analytics to comprehend customer preferences, optimize menus, and enhance operational efficiency. This analytical approach facilitates continuous improvement and adaptation to evolving market trends. Although cloud kitchens do not require prominent retail locations, their placement is strategically chosen based on areas with higher requirements for food delivery services, contributing to their operational success. Cloud kitchens frequently collaborate with third-party delivery platforms such as Uber Eats, DoorDash, or local equivalents. This partnership expands their reach and enables them to tap into a broader customer base.

Get an overview of this study by requesting a free sample

Rising Demand for Food Delivery Services - The increasing preference for online food ordering and delivery services has propelled the demand for cloud kitchens. Consumers' busy lifestyles and the convenience of ordering meals through mobile apps have fueled the growth of food delivery platforms.

Cost-Efficiency and Lower Operational Overheads - Cloud kitchens operate with lower upfront costs and reduced operational overheads compared to traditional brick-and-mortar restaurants. This cost-effectiveness attracts entrepreneurs and existing food businesses to adopt cloud kitchen models, allowing them to focus on culinary innovation and marketing.

Rapidly Changing Consumer Preferences and Food Trends - Cloud kitchens can easily adapt to changing consumer preferences and emerging food trends due to their agile and flexible operational structure. The ability to experiment with diverse cuisines and menu options enables cloud kitchens to cater to evolving tastes and preferences.

Dependence on Third-Party Delivery Platforms - Cloud kitchens often rely heavily on third-party delivery services, subjecting them to these platforms' policies, fees, and commission structures. High commission rates charged by delivery aggregators can impact the profitability of cloud kitchens and limit their control over the end-to-end customer experience.

Intense Competition and Saturation - The increasing popularity of cloud kitchens has led to a surge in competition, resulting in market saturation in certain regions. Additionally, intense competition may lead to pricing pressures and reduced profit margins for cloud kitchen operators.

Data-Driven Decision Making - Leveraging data analytics and customer insights allows cloud kitchens to make informed decisions regarding menu optimization, pricing strategies, and marketing initiatives, enhancing overall operational efficiency.

Partnerships with Delivery Aggregators - Collaborating with delivery aggregators and establishing strategic partnerships can broaden the reach of cloud kitchens, tapping into the expansive customer bases of these platforms and driving additional sales.

Global Expansion and Market Penetration - The scalability of cloud kitchen models facilitates global expansion, allowing operators to enter new markets with relative ease. This opportunity enables brands to tap into diverse consumer demographics and preferences worldwide.

Operational Complexities and Quality Control - Managing multiple virtual brands within a single kitchen space can pose operational challenges. Ensuring consistent food quality across diverse cuisines and meeting customer expectations adds complexity to the day-to-day operations of cloud kitchens.

High Dependency on Digital Platforms - Cloud kitchens heavily rely on digital platforms for order processing and delivery. However, dependence on third-party aggregators can lead to increased costs, commission pressures, and potential loss of control over customer interactions.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific emerged as the most prominent global Cloud Kitchen market, with a 61.13% market revenue share in 2022.

The Asia Pacific region has witnessed rapid urbanization, leading to a shift in consumer lifestyles. Busy urban populations increasingly seek convenient food solutions, driving the need for online food delivery services provided by cloud kitchens. The Asia Pacific region is home to a large, tech-savvy population that readily embraces digital platforms for various services, including food delivery. The widespread use of smartphones and increasing internet penetration have facilitated the adoption of cloud kitchen services. In addition, the growing middle-class population in countries across the Asia Pacific region has increased spending capacity on food services. Cloud kitchens, offering a variety of cuisines at various price points, cater to the diverse preferences of this expanding consumer segment. North America has secured a substantial market share in the cloud kitchen market in 2022. North America has a well-established food delivery and takeout culture, with consumers accustomed to ordering meals for home consumption. The convenience offered by cloud kitchens aligns with this cultural preference for off-premise dining. Furthermore, the availability of investment and funding opportunities has played a crucial role in North America's growth of cloud kitchens. Investors and venture capitalists have shown significant interest in supporting innovative food delivery models. Additionally, cloud kitchens in North America often form strategic partnerships with established food delivery platforms. This collaboration enhances their reach, tapping into the extensive customer bases of these platforms and driving additional sales.

Asia Pacific Region Cloud Kitchen Market Share in 2022 - 61.13%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The type segment is classified into commissary/shared kitchen, independent cloud kitchen and kitchenpods. The independent cloud kitchen segment dominated the market, with a share of around 62.53% in 2022. Independent cloud kitchens operate with a high degree of agility and flexibility. Unlike traditional brick-and-mortar restaurants or franchise models, they can quickly adapt to changing consumer preferences, experiment with new cuisines, and adjust their menus without the constraints of a physical storefront or corporate structure. Independent cloud kitchens typically have lower operational overheads and require a lower initial investment compared to establishing a traditional restaurant. This financial advantage allows entrepreneurs and small business owners to enter the food industry with reduced financial risks. Furthermore, the independent nature of these cloud kitchens fosters an entrepreneurial spirit. Entrepreneurs can bring innovative culinary concepts to the market without the bureaucratic processes associated with larger restaurant chains. This creativity contributes to the diversity and uniqueness of offerings, attracting a broader customer base.

The nature segment includes franchised and standalone. In 2022, the franchised segment dominated the market with the largest share of 63.18%. Franchised cloud kitchens often leverage established brand names. This recognition can attract customers, as consumers may be more inclined to order from a familiar brand, even in the virtual kitchen space. Franchises typically operate based on proven business models. This factor includes standardized processes, recipes, and operational guidelines. Such consistency can contribute to customer trust and loyalty, as they expect a reliable experience regardless of the location. Besides, franchising offers entrepreneurs a lower-risk entry into the cloud kitchen market. They can tap into the success of an established brand with a track record, reducing the indecisiveness associated with beginning a business from scratch.

The product segment is divided into burger/sandwich, chicken, Mexican/Asian food, pizza, pasta, seafood and others. The burger/sandwich segment dominated the market, with a share of around 27.39% in 2022. Burgers and sandwiches have a universal appeal and are familiar to a broad range of consumers. These products are comfort foods enjoyed by people across different cultures, making them a safe and popular choice in the cloud kitchen market. Burgers and sandwiches are well-suited for delivery as they can retain their quality and taste during transit. Their structure allows for easy packaging, ensuring customers receive a satisfactory product even when ordering online. In addition, the burger and sandwich categories offer extensive customization options. Cloud kitchens can experiment with diverse ingredients, flavours, and culinary styles, allowing a wide range of offerings catering to different tastes and preferences.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2022 | USD 58.61 Billion |

| Market size value in 2032 | USD 177.85 Billion |

| CAGR (2023 to 2032) | 11.74% |

| Historical data | 2019-2021 |

| Base Year | 2022 |

| Forecast | 2023-2032 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East & Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Type, Nature, and Product |

As per The Brainy Insights, the size of the cloud kitchen market was valued at USD 58.61 billion in 2022 to USD 177.85 billion by 2032.

The global cloud kitchen market is growing at a CAGR of 11.74% during the forecast period 2023-2032.

Asia Pacific became the largest market for cloud kitchen.

The rising demand for food delivery services, changing consumer preferences and food trends drive the market's growth.

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. The Brainy Insights has segmented the global Cloud Kitchen market based on below-mentioned segments:

Global Cloud Kitchen Market by Type:

Global Cloud Kitchen Market by Nature:

Global Cloud Kitchen Market by Product:

Global Cloud Kitchen Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date