- +1-315-215-1633

- sales@thebrainyinsights.com

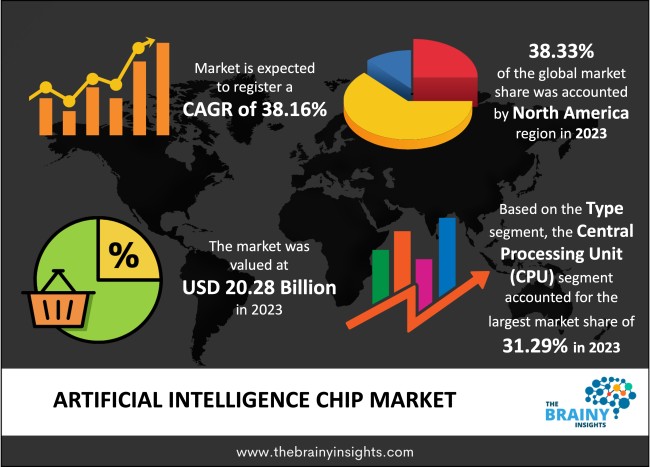

The global Artificial Intelligence Chip market generated USD 20.28 billion revenue in 2023 and is projected to grow at a CAGR of 38.16% from 2024 to 2033. The market is expected to reach USD 513.97 billion by 2033. The surge in demand for deep learning and the widespread integration of artificial intelligence (AI) across diverse industries are key drivers fueling the expansion of the artificial intelligence chip market. Additionally, a notable uptick in investments directed toward research and development (R&D) initiatives aimed at uncovering cutting-edge AI chip technologies has significantly contributed to the global growth of this market. The evolution of technology, particularly the increased deployment of robotics across various sectors, has acted as a catalyst, further propelling the demand for the artificial intelligence chip market.

AI chips, or artificial intelligence chips, are specialized hardware components designed to process and execute tasks related to artificial intelligence (AI) and machine learning (ML) applications. These chips play a crucial role in accelerating the performance of AI algorithms, enabling faster and more efficient processing of complex computations. AI chips are integral to the advancement of AI technologies across various industries. Their development and utilization have become pivotal in meeting the growing demand for sophisticated AI applications. As industries such as healthcare, retail, finance, and automotive increasingly adopt AI for data analysis, pattern recognition, and decision-making processes, the significance of AI chips in driving innovation and efficiency continues to grow. The relentless pursuit of enhancing AI capabilities has led to increased investments in research and development, aiming to create more powerful and energy-efficient AI chips. This ongoing innovation contributes to the evolution of AI chip architectures, pushing the boundaries of computational efficiency and enabling the development of advanced AI models. Moreover, the synergy between AI chips and emerging technologies like quantum computing is on the horizon, promising to unlock new possibilities in handling large datasets and optimizing operational processes. As the demand for AI applications expands, the role of AI chips remains pivotal in shaping the future landscape of artificial intelligence, driving advancements that have far-reaching implications for industries and society.

Get an overview of this study by requesting a free sample

Increasing Demand for Edge Computing - The growing use of edge computing, where data processing ensues closer to the source of data generation rather than depending solely on centralized cloud servers, fuels the demand for AI chips. Edge devices require efficient and powerful AI processing to handle real-time applications and reduce latency.

Growing Data Volume and Complexity - The explosion of big data and the increasing complexity of data sets drive the need for faster and more efficient processing. AI chips are designed to handle the massive amounts of data involved in training and executing complex machine learning (ML) models.

Rapid Advancements in AI Technologies - The continuous evolution and advancement of AI applications and technologies, including deep learning (DL) and machine learning (ML), are significant drivers. As artificial intelligence algorithms become more complicated, there is a growing demand for specialized hardware acceleration, leading to increased adoption of AI chips.

High Development Costs - The research, development, and manufacturing of advanced AI chips involve substantial costs. High initial investment is a barrier for smaller companies and startups to enter the market, limiting overall competition.

Complexity of Integration - Integrating AI chips into existing systems can be complex, especially in industries with legacy infrastructure. Compatibility issues and the need for system redesign may slow the adoption of AI chips in certain applications.

Increased Adoption in Healthcare - AI chips offer significant opportunities in the healthcare sector, including medical imaging, diagnostics, drug discovery, and personalized medicine. AI in healthcare is expected to drive the demand for specialized chips tailored to medical applications.

Expansion in Autonomous Vehicles- The development and deployment of autonomous vehicles represent a substantial opportunity for AI chip manufacturers. These chips are crucial in processing sensor data and enabling real-time decision-making for safe and efficient autonomous driving.

Edge AI for IoT Devices - The proliferation of IoT devices creates a demand for AI processing at the edge to enhance device intelligence and efficiency. AI chips designed for edge computing open opportunities for applications in smart homes, industrial IoT, and more.

Regulatory and Ethical Concerns - Increasing scrutiny and evolving regulations regarding data privacy, bias, and ethical considerations in AI applications pose challenges. Compliance with diverse global regulations and ensuring ethical use of AI technology are ongoing concerns for the industry.

Global Supply Chain Disruptions - The semiconductor industry, including AI chip manufacturing, is vulnerable to global supply chain disruptions. Events like geopolitical tensions, natural disasters, or pandemics can impact production and lead to shortages.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most prominent global Artificial Intelligence Chip market, with a 38.33% market revenue share in 2023.

North America, particularly Silicon Valley in California, is a global hub for technological innovation. The presence of leading technology companies, startups, research institutions, and venture capital firms fosters an environment conducive to developing cutting-edge AI chip technologies. Some of the world's biggest technology organizations, including those at the forefront of AI development, are headquartered in North America. Companies like Intel, NVIDIA, AMD, Google, and IBM have played pivotal roles in advancing AI chip technologies, contributing to the region's dominance. Furthermore, the region attracts significant investments in AI research and development. Both private and public funding supports initiatives focused on advancing AI technologies, including developing specialized hardware such as AI chips. Additionally, North America benefits from a robust ecosystem that encourages collaboration between academia, industry, and government. Research institutions collaborate with tech companies, fostering the exchange of ideas and accelerating the pace of AI chip innovation. The region also has been an early adopter of AI technologies in various industries, including healthcare, finance, autonomous vehicles, and more. This early adoption has driven the demand for advanced AI chips, and North American companies have been at the forefront of meeting these requirements. Besides, tech companies in North America often engage in strategic alliances, partnerships, and acquisitions to strengthen their positions in the AI chip market. These collaborations contribute to the development of comprehensive AI solutions.

North America Region Artificial Intelligence Chip Market Share in 2023 - 38.33%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The type segment is classified into application-specific integrated circuit (ASIC), central processing unit (CPU), field programmable gate array (FPGA), graphics processing unit (GPU) and others. The central processing unit (CPU) segment dominated the market, with a share of around 31.29% in 2023. Central Processing Units (CPUs) are general-purpose processors designed to handle a wide range of tasks. They can efficiently execute diverse instructions, making them suitable for various applications involving AI. CPUs also have been integral components of traditional computing systems for decades. Many existing systems and applications are built around CPU architectures, creating a foundation for their continued use in AI tasks. In addition, CPUs are compatible with a broad range of software, and many AI applications and frameworks are developed to run on standard CPU architectures. This compatibility simplifies the deployment of AI models on existing infrastructure.

The processing type segment is split into cloud and edge. The edge segment dominated the market, with a share of around 74.45% in 2023. Many AI applications, especially those involving IoT devices, autonomous systems, and critical infrastructure, require real-time processing. By bringing computational resources closer to the point of data generation, edge computing addresses latency concerns and supports real-time decision-making. Edge computing further reduces the need to transmit extensive volumes of data to centralized cloud servers for processing. This characteristic lowers bandwidth requirements and minimizes the impact on network infrastructure, making edge computing more bandwidth-efficient. Additionally, edge computing allows sensitive data to be processed locally on devices, enhancing privacy and data security. This factor is particularly important in healthcare, finance, and surveillance applications, where strict privacy regulations must be followed.

The technology segment is divided into system on chip, system in package, multi-chip module and others. The system on chip segment dominated the market, with a share of around 37.21% in 2023. System-on-chips (SoCs) integrate various components onto a single chip, including processors, memory, accelerators, and other peripherals. This integration enhances overall system efficiency and reduces the need for separate components, making SoCs cost-effective. Further, the compact design of SoCs makes them space-efficient, making them suitable for use in devices with limited physical space, such as smartphones, edge devices, and IoT devices. Additionally, integrating components onto a single chip contributes to power efficiency. Many SoCs, including AI, are designed and optimized for specific applications or use cases. Customization allows SoCs to deliver high performance for targeted workloads, making them ideal for edge devices and other applications requiring specialized AI.

The application segment includes computer vision, nature language processing, network security, robotics and others. The nature language processing segment dominated the market, with a share of around 30.21% in 2023. Many Natural Language Processing (NLP) algorithms are highly parallelizable, especially those based on deep learning models like recurrent neural networks (RNNs) and transformers. GPUs, in particular, excel at parallel processing, allowing them to perform NLP computations faster and more efficiently. Moreover, developing and using large pre-trained language models, such as Bidirectional Encoder Representations from Transformers and Generative Pre-trained Transformers, have become prevalent in NLP. These models demand substantial computational power, and AI chips optimized for these workloads are crucial for efficient deployment. Besides, the proliferation of voice-activated devices and applications relies heavily on NLP. AI chips optimized for speech recognition and natural language understanding are essential in devices like smart speakers, voice assistants, and other voice-activated technologies.

The industry vertical segment is divided into automotive and transportation, BFSI, healthcare, IT and telecom, media and advertising, retail and others. The BFSI segment dominated the market, with a share of around 22.65% in 2023. The BFSI sector deals with vast data, including customer transactions, market trends, and risk analysis. AI chips are instrumental in efficiently processing and analyzing this data, enabling real-time insights for better decision-making. AI-driven applications powered by specialized chips are essential for fraud detection and enhancing cybersecurity in the BFSI sector. AI algorithms can identify anomalous patterns and potential security threats, contributing to improved fraud prevention measures. Additionally, AI applications, particularly chatbots and virtual assistants, are widely used in the BFSI sector to enhance customer service and streamline interactions. AI chips play a role in efficiently processing natural language queries and providing quick, automated responses.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2023 | USD 20.28 Billion |

| Market size value in 2033 | USD 519.37 Billion |

| CAGR (2024 to 2033) | 38.16% |

| Historical data | 2020-2022 |

| Base Year | 2023 |

| Forecast | 2024-2033 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East & Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Type, Processing Type, Technology, Application and Industry Vertical |

As per The Brainy Insights, the size of the artificial intelligence chip market was valued at USD 20.28 billion in 2023 to USD 513.97 billion by 2033.

The global artificial intelligence chip market is growing at a CAGR of 38.16% during the forecast period 2024-2033.

North America became the largest market for artificial intelligence chip.

increasing demand for edge computing drives the market's growth.

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global Artificial Intelligence Chip market based on below-mentioned segments:

Global Artificial Intelligence Chip Market by Type:

Global Artificial Intelligence Chip Market by Processing Type:

Global Artificial Intelligence Chip Market by Technology:

Global Artificial Intelligence Chip Market by Application:

Global Artificial Intelligence Chip Market by Industry Vertical:

Global Artificial Intelligence Chip Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date