- +1-315-215-1633

- sales@thebrainyinsights.com

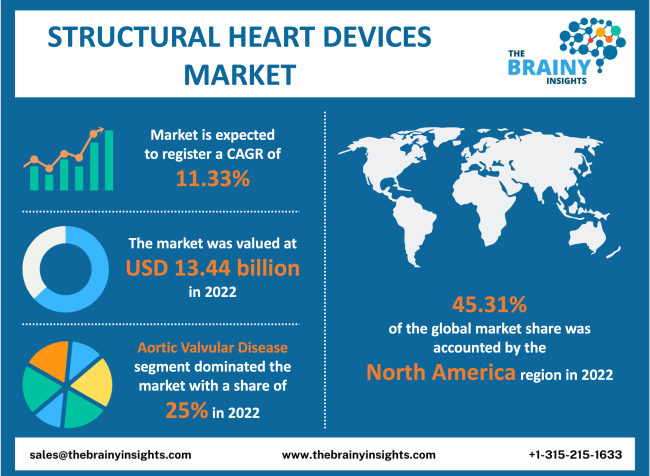

The global structural heart devices market is expected to grow from USD 13.44 billion in 2022 to USD 31.71 billion by 2030, at a CAGR of 11.33% during the forecast period 2022-2030. The North American structural heart devices market is expected to maintain its dominance during the forecast period.

The heart is an extremely vital organ of the body. It pumps the blood to keep the other organs functioning. It pumps blood continuously without a break, making it extremely important to keep it healthy. However, with the lifestyle changes associated with a lack of physical exercise and unhealthy foods, heart disease has increased. Similarly, other factors, such as increasing consumption of alcohol and substance abuse, are also increasing the number of heart patients. Structural heart diseases are associated with damage to the heart's walls, valves, muscles and chambers. Such damage restricts the blood flow and causes chest pains and fatigue. Smoking, alcohol consumption and high-dose medications during pregnancy have increased the incidence of congenital heart disease in infants. Similar habits in adults have caused a spike in congenital heart disease cases. Other structural heart diseases have also witnessed a rise globally. Structural heart devices are used to repair or replace the heart's damaged walls, chambers, valves or muscles. They are placed in the heart and improve blood flow. The minimally invasive nature of surgeries associated with these devices improves patient outcomes and offers them longevity. Their quality of life is improved. The advancement in medicine will further the development of the global structural heart devices market.

Get an overview of this study by requesting a free sample

December 2022 - The latest generation transcatheter aortic valve implantation (TAVI) technology, Navitor, has been made available by global healthcare giant Abbott for patients in India who have severe aortic stenosis and are at high or extremely high risk for surgery. Innovating with a special design to stop blood from leaking around the valve, the Navitor valve manufacturer claims to be enhancing transcatheter aortic valve replacement (TAVI or TAVR) therapies. According to the business, the Navitor TAVI system is the most recent addition to its extensive structural heart transcatheter portfolio. It provides doctors and patients with less invasive solutions for treating heart disorders. According to the manufacturer, TAVI offers patients with this crippling ailment a less intrusive option to surgical aortic valve replacement that can lessen symptoms and enhance the quality of life.

December 2022 - A multi-centre, first-of-its-kind national clinical trial for the LAmbre Plus Left Atrial Appendage Closure System, a left atrial appendage occlusion device, will be led by Henry Ford Health in Detroit. Left atrial appendage closure is a therapy method used to lower the risk that blood clots from the left atrial appendage would enter the bloodstream and result in a stroke. In individuals with non-valvular atrial fibrillation, LAAO devices are implanted in the heart to lower the risk of thromboembolism from the left atrial appendage (LAA). The systemic circulation, which transports oxygenated blood from the left ventricle through the arteries to the capillaries in the body's tissues, is prevented from being affected by LAA thrombus, a condition frequently linked to atrial fibrillation or AFib, by the device's mechanical occlusion of the LAA. The FDA gave the trial the go-ahead in March, and the Centers for Medicare and Medicaid Services did the same in August. The approvals allow patients to sign up for clinical research and receive full coverage from American health insurance companies.

The rising incidence of structural heart diseases – structural heart diseases are diseases that affect the heart muscles, valves, walls or chambers. Cardiomyopathy, heart valve diseases and congenital heart diseases are common structural heart diseases. Structural heart diseases are found in infants and they can also develop with age. There has been an increasing incidence of structural heart diseases. For instance, around 1 billion infants suffer from congenital heart diseases and around the same number of adults develop this disease annually in the USA. Similarly, several thousand people suffer from cardiomyopathy. While ill effects of certain medications, alcohol and drug use during smoking can cause congenital heart disease in infants, it can also develop with age if there is substance abuse or heavy alcohol consumption. The growing trend of using alcohol, smoking and medication to relieve stress has increased the population's risk of structural heart disease. Similarly, the increasing instances of heart attacks have increased the population's vulnerability towards structural heart diseases. Hypertension, high blood pressure, autoimmune diseases, and other conditions are also contributing to the rise in structural heart disease patients. Therefore, the increasing incidence of structural heart diseases will drive the global structural heart device market.

Structural heart devices are expensive – Billions are invested in developing sophisticated diagnostic and treatment procedures. The medical equipment devices, medications and personnel are high-cost inputs involved in the development of any treatment or product. However, every new device or medication being tested does not necessarily guarantee successful or full-proof results. Significant capital is lost behind these failed attempts at improving medicine. The successful ones also have invested a lot of money. Structural heart device research and development is time-consuming and expensive. The money invested in the research and development of successful projects must be realized when the product is commercialized to continue creating new treatments or devices. Therefore, the market players charge large sums for these sophisticated, high-end, and effective structural heart devices. The market's expansion will be constrained by how expensive structural heart devices are.

Technological advancements and increasing research and development expenditure – the increasing incidence of structural heart diseases has prompted government institutions worldwide to increase research and development expenditure to improve the nations' diagnostic and treatment infrastructure. Technological advancements have enabled the medical sector to develop enhanced medical devices, medications, therapies and treatments that are effective, low-cost and accessible to the population. The improved global healthcare over the decades has allowed pharmaceutical and biotechnology companies to shift their focus towards diagnostics and treatments of otherwise neglected conditions. Therefore, technological advancements and increasing research and development expenditure have improved the diagnostic and treatment infrastructure for structural heart diseases. The improvement is bound to continue and offer lucrative opportunities to the market players in the global structural heart devices market.

Stringent regulatory guidelines – as much as structural heart devices can improve the patient's life and longevity, they can be harmful if they are not subjected to proper scrutiny during approval or monitoring of their commercial use. These devices have the potential to directly impact the patients and cause significant and irreversible damage. Lax regulations and guidelines can lead to unavoidable deaths. Therefore, stringent guidelines govern the approval of structural heart devices and monitoring of their use afterwards to safeguard consumer interests. There are national institutions in place that implement these rules and guidelines. They are responsible for the citizenry and hold the big pharma companies accountable in case of negligence. Such stringency can cause a delay in approvals which is detrimental to the company's business and might discourage them from undertaking projects that further medicine. The stringent government regulations will challenge the growth of the market.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. The North American region emerged as the largest global structural heart devices market, with a 45.31% market revenue share in 2022. One of the main drivers of the industry is the existence of a sizable population that suffers from structural heart diseases. Early detection of structural heart diseases is made possible by the well-established healthcare infrastructure, which also has a sophisticated and large diagnostics network. Quick access to treatments is also provided. The disease's increased prevalence will also aid the market's growth in the middle-aged population. Early diagnosis and treatment of infant congenital heart disease are made possible by well-established paediatric care, which is an important secondary driver. Structural heart device research and development is the main focus of major pharmaceutical and biotechnology firms. A strong scientific community and a strong research infrastructure have produced a number of scientific advancements that have opened the door to developing sophisticated, minimally invasive and highly effective structural heart devices. The extensive insurance protection system and public healthcare programmes aid the market's expansion.

North America Region Structural Heart Devices Market Share in 2022 - 45.31%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The indication segment is divided into atrial septal defects, aortic valvular disease, pulmonary valvular disease, patent foramen ovale, ventricular septal defects, mitral valvular disease, patent ductus arteriosus, and others. The aortic valvular disease segment dominated the market with a market share of around 25% in 2022. AorticAs the name suggests, the aortic valvular disease is associated with the aorta. Aorta is the artery that is responsible for carrying the oxygenated blood from the heart to the rest of the body. In aortic valvular disease, the aorta does not open fully. The constricted blood flow caused by the incomplete relaxation of the aorta wall/muscles leads to a low amount of oxygen reaching the rest of the body. The heart has to work harder to transport oxygen. This leads to chest pain and fatigue. Aortic valvular disease is very common in the world. It is treated by placing a structural heart device via minimally invasive surgical procedures. Therefore, aortic valvular disease will dominate the indication segment.

The product segment is divided into heart valve devices, annuloplasty rings, occluders and delivery systems, transcatheter mitral valve repair, and others. The heart valve devices segment dominated the market with a market share of around 45% in 2022. Heart valve devices treat any type of heart valve disease that might have to constrict or damage the valve. These devices are highly durable and can be placed in the body with minimally invasive surgical procedures. They improve the blood flow and longevity of the patients. They enhance the quality of life of the patient. The demand for heart valve devices has increased with the rising number of heart valve diseases. It has also increased as a treatment option, given the positive reimbursement policies of the government with wide coverage.

The procedure segment is divided into repair and replacements. The replacement segment dominated the market with a market share of around 65% in 2022. Structural heart diseases degrade the quality of life with constant chest pains and fatigue. The repairs performed by administering medications or surgical interventions do not fully guarantee the longevity of the treatment. The effectiveness of repairs also decreases with time, causing the patient to go through the same stress again. With the advent of better, flexible, advanced, durable and highly effective structural heart devices, the demand for replacement has increased. Replacement improves the blood flow and offers the patient a chance for a longer life. Replacement is a successful long-term solution to repair procedures.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2022 | USD 13.44 Billion |

| Market size value in 2030 | USD 31.71 Billion |

| CAGR (2022 to 2030) | 11.33% |

| Historical data | 2019-2020 |

| Base Year | 2021 |

| Forecast | 2022-2030 |

| Segments | The research segment is based on the indication, product and procedure. |

| Regional Segments | The regions examined for the market are Europe, Asia Pacific, North America, South America, and Middle East & Africa. |

As per The Brainy Insights, the size of the structural heart devices market was valued at USD 13.44 billion in 2022 to USD 31.71 billion by 2030.

Global structural heart devices market is growing at a CAGR of 11.33% during the forecast period 2022-2030.

The market's growth will be influenced by the rising incidence of structural heart diseases.

Structural heart devices are expensive and that could hamper the market growth.

1. Introduction

1.1. Objectives of the Study

1.2. Market Definition

1.3. Research Scope

1.4. Currency

1.5. Key Target Audience

2. Research Methodology and Assumptions

3. Executive Summary

4. Premium Insights

4.1. Porter’s Five Forces Analysis

4.2. Value Chain Analysis

4.3. Top Investment Pockets

4.3.1. Market Attractiveness Analysis by Indication

4.3.2. Market Attractiveness Analysis by Product

4.3.3. Market Attractiveness Analysis by Procedure

4.3.4. Market Attractiveness Analysis by Region

4.4. Industry Trends

5. Market Dynamics

5.1. Market Evaluation

5.2. Drivers

5.2.1. The rising incidence of structural heart diseases

5.3. Restraints

5.3.1. Structural heart devices are expensive

5.4. Opportunities

5.4.1. Technological advancements and increasing research and development expenditure

5.5. Challenges

5.5.1. Stringent regulatory guidelines

6. Global Structural Heart Devices Market Analysis and Forecast, By Indication

6.1. Segment Overview

6.2. Atrial Septal Defects

6.3. Aortic Valvular Disease

6.4. Pulmonary Valvular Disease

6.5. Patent Foramen Ovale

6.6. Ventricular Septal Defects

6.7. Mitral Valvular Disease

6.8. Patent Ductus Arteriosus

6.9. Others

7. Global Structural Heart Devices Market Analysis and Forecast, By Product

7.1. Segment Overview

7.2. Heart Valve Devices

7.3. Annuloplasty Rings

7.4. Occluders and Delivery Systems

7.5. Transcatheter Mitral Valve Repair

7.6. Others

8. Global Structural Heart Devices Market Analysis and Forecast, By Procedure

8.1. Segment Overview

8.2. Repair

8.3. Replacement

9. Global Structural Heart Devices Market Analysis and Forecast, By Regional Analysis

9.1. Segment Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.4. Asia-Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.5. South America

9.5.1. Brazil

9.6. Middle East and Africa

9.6.1. UAE

9.6.2. South Africa

10. Global Structural Heart Devices Market-Competitive Landscape

10.1. Overview

10.2. Market Share of Key Players in the Structural Heart Devices Market

10.2.1. Global Company Market Share

10.2.2. North America Company Market Share

10.2.3. Europe Company Market Share

10.2.4. APAC Company Market Share

10.3. Competitive Situations and Trends

10.3.1. Product Launches and Developments

10.3.2. Partnerships, Collaborations, and Agreements

10.3.3. Mergers & Acquisitions

10.3.4. Expansions

11. Company Profiles

11.1. Abbott

11.1.1. Business Overview

11.1.2. Company Snapshot

11.1.3. Company Market Share Analysis

11.1.4. Company Product Portfolio

11.1.5. Recent Developments

11.1.6. SWOT Analysis

11.2. Boston Scientific Corporation

11.2.1. Business Overview

11.2.2. Company Snapshot

11.2.3. Company Market Share Analysis

11.2.4. Company Product Portfolio

11.2.5. Recent Developments

11.2.6. SWOT Analysis

11.3. CryoLife

11.3.1. Business Overview

11.3.2. Company Snapshot

11.3.3. Company Market Share Analysis

11.3.4. Company Product Portfolio

11.3.5. Recent Developments

11.3.6. SWOT Analysis

11.4. Edwards Lifesciences Corporation

11.4.1. Business Overview

11.4.2. Company Snapshot

11.4.3. Company Market Share Analysis

11.4.4. Company Product Portfolio

11.4.5. Recent Developments

11.4.6. SWOT Analysis

11.5. JenaValve Technology Inc.

11.5.1. Business Overview

11.5.2. Company Snapshot

11.5.3. Company Market Share Analysis

11.5.4. Company Product Portfolio

11.5.5. Recent Developments

11.5.6. SWOT Analysis

11.6. Lepu Medical Technology

11.6.1. Business Overview

11.6.2. Company Snapshot

11.6.3. Company Market Share Analysis

11.6.4. Company Product Portfolio

11.6.5. Recent Developments

11.6.6. SWOT Analysis

11.7. LivaNova PLC

11.7.1. Business Overview

11.7.2. Company Snapshot

11.7.3. Company Market Share Analysis

11.7.4. Company Product Portfolio

11.7.5. Recent Developments

11.7.6. SWOT Analysis

11.8. Medtronic PLC

11.8.1. Business Overview

11.8.2. Company Snapshot

11.8.3. Company Market Share Analysis

11.8.4. Company Product Portfolio

11.8.5. Recent Developments

11.8.6. SWOT Analysis

11.9. Micro Interventional Devices

11.9.1. Business Overview

11.9.2. Company Snapshot

11.9.3. Company Market Share Analysis

11.9.4. Company Product Portfolio

11.9.5. Recent Developments

11.9.6. SWOT Analysis

11.10. St. Jude Medical

11.10.1. Business Overview

11.10.2. Company Snapshot

11.10.3. Company Market Share Analysis

11.10.4. Company Product Portfolio

11.10.5. Recent Developments

11.10.6. SWOT Analysis

List of Table

1. Global Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

2. Global Atrial Septal Defects Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

3. Global Aortic Valvular Disease Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

4. Global Pulmonary Valvular Disease Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

5. Global Patent Foramen Ovale Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

6. Global Ventricular Septal Defects Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

7. Global Mitral Valvular Disease Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

8. Global Patent Ductus Arteriosus Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

9. Global Others Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

10. Global Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

11. Global Heart Valve Devices Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

12. Global Annuloplasty Rings Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

13. Global Occluders and Delivery Systems Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

14. Global Transcatheter Mitral Valve Repair Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

15. Global Others Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

16. Global Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

17. Global Repair Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

18. Global Replacement Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

19. Global Structural Heart Devices Market, By Region, 2019-2030 (USD Billion)

20. North America Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

21. North America Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

22. North America Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

23. U.S. Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

24. U.S. Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

25. U.S. Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

26. Canada Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

27. Canada Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

28. Canada Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

29. Mexico Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

30. Mexico Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

31. Mexico Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

32. Europe Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

33. Europe Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

34. Europe Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

35. Germany Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

36. Germany Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

37. Germany Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

38. France Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

39. France Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

40. France Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

41. U.K. Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

42. U.K. Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

43. U.K. Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

44. Italy Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

45. Italy Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

46. Italy Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

47. Spain Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

48. Spain Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

49. Spain Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

50. Asia Pacific Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

51. Asia Pacific Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

52. Asia Pacific Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

53. Japan Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

54. Japan Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

55. Japan Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

56. China Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

57. China Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

58. China Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

59. India Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

60. India Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

61. India Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

62. South America Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

63. South America Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

64. South America Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

65. Brazil Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

66. Brazil Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

67. Brazil Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

68. Middle East and Africa Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

69. Middle East and Africa Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

70. Middle East and Africa Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

71. UAE Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

72. UAE Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

73. UAE Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

74. South Africa Structural Heart Devices Market, By Indication, 2019-2030 (USD Billion)

75. South Africa Structural Heart Devices Market, By Product, 2019-2030 (USD Billion)

76. South Africa Structural Heart Devices Market, By Procedure, 2019-2030 (USD Billion)

List of Figures

1. Global Structural Heart Devices Market Segmentation

2. Structural Heart Devices Market: Research Methodology

3. Market Size Estimation Methodology: Bottom-Up Approach

4. Market Size Estimation Methodology: Top-Down Approach

5. Data Triangulation

6. Porter’s Five Forces Analysis

7. Value Chain Analysis

8. Global Structural Heart Devices Market Attractiveness Analysis by Indication

9. Global Structural Heart Devices Market Attractiveness Analysis by Product

10. Global Structural Heart Devices Market Attractiveness Analysis by Procedure

11. Global Structural Heart Devices Market Attractiveness Analysis by Region

12. Global Structural Heart Devices Market: Dynamics

13. Global Structural Heart Devices Market Share by Indication (2022 & 2030)

14. Global Structural Heart Devices Market Share by Product (2022 & 2030)

15. Global Structural Heart Devices Market Share by Procedure (2022 & 2030)

16. Global Structural Heart Devices Market Share by Regions (2022 & 2030)

17. Global Structural Heart Devices Market Share by Company (2021)

This study forecasts revenue at global, regional, and country levels from 2019 to 2030. The Brainy Insights has segmented the structural heart devices market based on below mentioned segments:

Structural Heart Devices Market by Indication:

Structural Heart Devices Market by Product:

Structural Heart Devices Market by Procedure:

Structural Heart Devices Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date