- +1-315-215-1633

- sales@thebrainyinsights.com

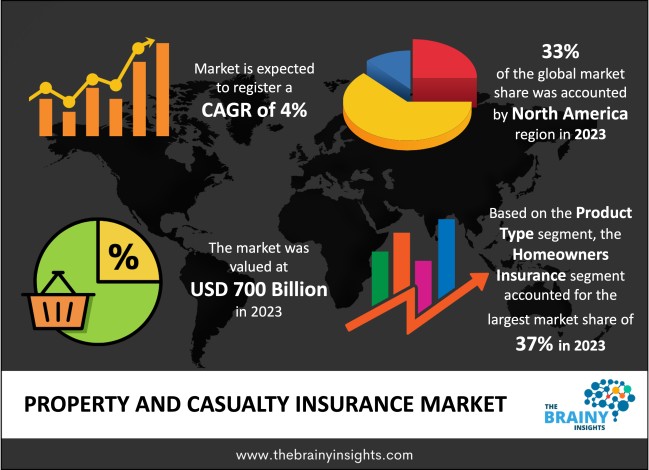

The global property and casualty insurance market was valued at USD 700 billion in 2023 and grew at a CAGR of 4% from 2024 to 2033. The market is expected to reach USD 1036.17 billion by 2033. The increasing infrastructural investments and stringent regulatory requirements will drive the growth of the global property and casualty insurance market.

Property and casualty insurance is commonly known as P&C insurance. It is a comprehensive insurance category that encompasses property and liability coverage. Property insurance protects against damage or loss of physical assets. The physical assets include homes, personal belongings, and business property, and casualty insurance covers legal responsibilities arising from injuries or damage to others. Individuals buy this insurance to protect their homes, while businesses buy it to safeguard physical assets, cover liability risks, and ensure business continuity. The need for property and casualty insurance arises from the inherent risks of owning or engaging in various activities. It offers financial security and peace of mind. Insurance policies provide the necessary funds to repair or replace damaged property, cover medical expenses, or settle legal liabilities. These insurance policies can be customized to meet specific needs according to the specific circumstances of consumers. Property and casualty insurance is vital in risk management, offering diverse coverage options for individuals and businesses.

Get an overview of this study by requesting a free sample

The increasing risk of climate change resulting in increasing instances of natural disasters – Climate change is contributing to a surge in both the frequency and severity of natural disasters, leading to increased property loss and loss of lives. The planet's warming climate intensifies extreme weather events, including hurricanes, floods, wildfires, and heatwaves. Rising global temperatures result in more frequent and intense storms, causing devastating impacts on communities, infrastructure, and ecosystems. The connection between climate change and natural disasters is evident in the escalating risks individuals and businesses face. These disasters, fueled by climate change, pose a direct threat to property, with damages ranging from structural losses to entire communities being displaced. The escalating risks and damages associated with climate-induced disasters drive a substantial increase in the demand for property and casualty insurance. Individuals and businesses recognize the imperative of financial protection against these events' unpredictable and intensified nature. As extreme weather events become more common, the need for insurance coverage to mitigate the economic fallout from property loss and liability claims is skyrocketing.

The high cost of premiums – High premiums, given the risk assessment process, claims history, and coverage limits, can make insurance unaffordable for individuals and businesses with limited financial resources. The complexity of premium calculations contributes to confusion and delays. The unaffordability and complex premium structures and calculations with hidden charges and conditionalities limit the adoption of property and casualty insurance.

The stringent legal requirements enforcing mandatory insurance coverage – Legal requirements mandating insurance coverage have increased public awareness about the importance of financial protection against property damage and liability claims. The increased number of insurance providers makes insurance options more diverse and affordable. Online platforms and insurance companies have made the insurance process more accessible, allowing consumers to research, compare, and purchase policies conveniently. Technological advancements have increased operational efficiency, coupled with data analyticsenablinges more accurate risk assessment.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global property and casualty insurance market, with a 33% market revenue share in 2023.

The region has one of the world's largest and most developed insurance markets, offering a diverse range of products to meet the varied needs of consumers. Regulatory stringency and stability offer a conducive environment for insurers to operate, ensuring consumer protection and industry stability. High income and asset levels and a cultural emphasis on financial security contribute to increased demand for insurance coverage in North America. Companies continually introduce new products and leverage advanced risk modelling, contributing to the regional market's growth and dominance globally.

North America Region Property and Casualty Insurance Market Share in 2023 - 33%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The product type segment is divided into homeowners insurance, condo insurance, car insurance, landlord insurance, renters insurance and others. The homeowners insurance segment dominated, with a market share of around 37% in 2023. Homeowners insurance protects homeowners from a range of potential financial losses related to their property, like the home's physical structure, personal property coverage for belongings, liability protection for injuries or property damage, additional living expense coverage, and medical payments coverage. It offers protection against unforeseen events like fires, storms, or theft. Mortgage lenders often require this type of insurance to ensure that the property serving as collateral is adequately protected. It also offers personal liability protection, covering legal claims and lawsuits arising from injuries or property damage for which the homeowner may be held responsible.

The distribution channel segment is divided into direct, agency, banks and others. The agency segment dominated the market, with a market share of around 46% in 2023. Insurance agencies serve as a key intermediary between insurance providers and consumers. These agencies are instrumental in making P&C insurance accessible and tailored to individual needs. Agents within these agencies leverage their expertise to assess client requirements, provide advice, and offer various insurance products, including homeowners, auto, and liability coverage. Insurance agencies customize solutions based on client risk profiles and financial situations. Agencies assist clients throughout the claims process, provide risk management services, and often have a local presence, enhancing their understanding of regional risks.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2023 | USD 700 Billion |

| Market size value in 2033 | USD 1036.17 Billion |

| CAGR (2024 to 2033) | 4% |

| Historical data | 2020-2022 |

| Base Year | 2023 |

| Forecast | 2024-2033 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Product Type and Distribution Channel |

As per The Brainy Insights, the size of the global property and casualty insurance market was valued at USD 700 billion in 2023 to USD 1036.17 billion by 2033.

Global property and casualty insurance market is growing at a CAGR of 4% during the forecast period 2024-2033.

The market's growth will be influenced by the increasing risk of climate change resulting in increasing instances of natural disasters.

The high cost of premiums could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global property and casualty insurance market based on below mentioned segments:

Global Property and Casualty Insurance Market by Product Type:

Global Property and Casualty Insurance Market by Distribution Channel:

Global Property and Casualty Insurance Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date