- +1-315-215-1633

- sales@thebrainyinsights.com

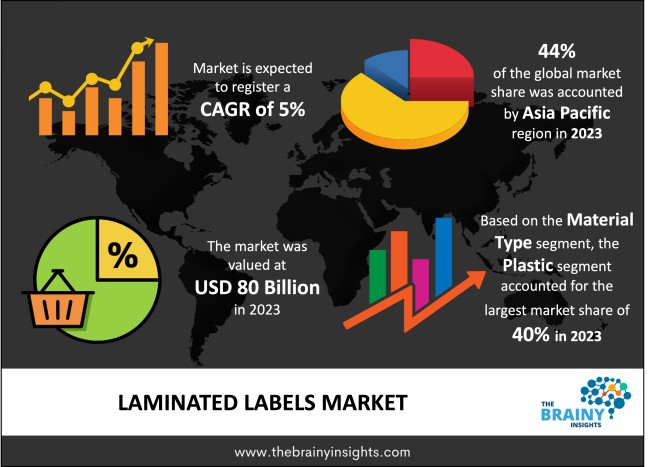

The global laminated labels market was valued at USD 80 billion in 2023 and grew at a CAGR of 5% from 2024 to 2033. The market is expected to reach USD 130.31 billion by 2033. The increasing demand for labelling across diverse industries will drive the growth of the global laminated labels market.

Laminated labels are labelling solutions consisting of multiple layers. It includes a base material, adhesive layer, and protective laminate. The base material is often paper or synthetic materials like vinyl or polyester, which provide the surface for printing essential information. An adhesive layer ensures secure attachment to various surfaces, while a protective laminate shields the label from environmental factors such as moisture, chemicals, abrasion, and UV radiation. Laminated labels convey crucial product information, including ingredients, usage instructions, and safety warnings. They ensure this information remains intact and legible throughout the product's lifecycle. Laminated labels are used in manufacturing, logistics, and warehousing to manage inventory efficiently. They are used in banners, posters, and signs, maintaining visibility and readability despite exposure to sunlight, rain, and other environmental factors. Moreover, laminated labels offer a professional appearance, enhancing the overall aesthetic appeal of products, packaging, and signage. Laminated labels play a vital role across industries, providing durable, visible, and protective labelling solutions.

Get an overview of this study by requesting a free sample

The increasing demand for labelling solutions across diverse industries – The growth and development of key industries such as food and beverage, pharmaceuticals, cosmetics, retail, industrial manufacturing, and logistics will significantly contribute to the increasing demand for laminated labels. The rising demand for packaged goods In the food and beverage industry will drive the need for durable and compliant labelling solutions like laminated labels. Similarly, expanding healthcare services will fuel the demand for laminated labels for pharmaceutical packaging and medical device labelling in the pharmaceutical and healthcare sectors. The cosmetics and personal care industry will require attractive, durable labelling solutions to enhance product presentation and brand differentiation. Adopting automation, digitalization, and Industry 4.0 technologies in industrial and manufacturing environments will lead to increased demand for robust labelling solutions for asset tracking, inventory management, and safety compliance. Therefore, the growth and development of these industries will drive the need for laminated labels as they play an integral role in these industries.

The cost of laminated labels – laminated labels require multiple layers of materials, such as a base substrate, adhesive, and laminate film, each contributing to the overall cost. Speciality laminates with features like UV resistance or tamper-evident properties may incur higher costs. The lamination process involves additional steps beyond standard label printing, including coating with adhesive and applying the laminate film, requiring specialized equipment, labour, and energy. The investment in lamination equipment further adds to the production costs, along with any specialized tools or accessories. Customization options, such as unique shapes, sizes, colours, and finishes, can increase costs due to additional setup time, design work, and printing adjustments. Advanced printing techniques or speciality inks for customized label designs may also increase expenses. Therefore, the costs of laminated labels will hamper the market’s growth.

Advancements and innovation in laminated labels – Manufacturers prioritise eco-friendly materials like biodegradable films and recyclable substrates to address sustainability concerns. These materials reduce environmental impact and meet regulatory requirements and consumer preferences for green packaging solutions. Enhancements in adhesive technology and laminate materials have significantly improved the durability of laminated labels. These labels offer better resistance to abrasion, chemicals, moisture, and UV radiation, ensuring longevity and legibility even in harsh environmental conditions. Additionally, integrating smart technologies like RFID and NFC enables functionalities such as real-time tracking, authentication, and interactive engagement with consumers, enhancing supply chain visibility and consumer experiences. Laminated labels now feature advanced anti-counterfeiting features such as holographic foils and tamper-evident seals, bolstering product security and brand protection. Moreover, advancements in printable electronics technology allow for integrating electronic components like sensors into laminated labels, enabling temperature monitoring and interactive packaging. These advancements will contribute to the market’s growth and development during the forecast period.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific emerged as the most significant global laminated labels market, with a 44% market revenue share in 2023.

The region's rapidly growing economies, such as China, India, and Southeast Asian countries, drive demand for packaged goods across various sectors, including food, beverages, cosmetics, and pharmaceuticals. With increasing industrialization, urbanization, and rising consumer purchasing power, the demand for laminated labels for branding and information dissemination is rising. Asia Pacific's food and beverage sector is expanding significantly, fueled by changing lifestyles and preferences. Urban consumers, in particular, seek convenience and a diverse range of packaged products, leading to heightened demand for laminated labels to enhance product presentation. Similarly, the pharmaceutical industry in the region is experiencing rapid growth due to increasing healthcare awareness and government initiatives to improve healthcare access. Laminated labels are crucial for pharmaceutical packaging. Technological advancements in printing and labelling have further propelled Asia Pacific's dominance in the laminated labels market.

Asia Pacific Region Laminated Labels Market Share in 2023 - 44%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The material type segment is divided into polyester, vinyl, polycarbonate, polypropylene, and others. The polyester segment dominated the market, with a market share of around 37% in 2023. Polyester is a synthetic polymer known for its durability. Polyester offers robust resistance against tearing, abrasion, and moisture, ensuring labels remain intact and legible in extreme environmental conditions. Its chemical resistance safeguards printed information from degradation when exposed to various substances, making it invaluable in the pharmaceutical, chemical, and automotive sectors. Moreover, polyester's wide temperature tolerance enables laminated labels to endure extreme heat or cold without compromising adhesion or integrity. Polyester's clarity and printability enable high-quality graphics, text, and barcodes, ensuring superior print resolution and readability on laminated labels. Its dimensional stability prevents shrinkage or expansion, maintaining label shape and size over time for accurate placement and readability. Polyester's UV resistance also protects against sunlight-induced fading or discolouration, ensuring labels retain their visual appeal in outdoor applications. Therefore, the numerous advantages of polyester in laminated labels contribute to its dominance in the market.

The form segment is divided into rolls and sheets. The rolls segment dominated the market, with a market share of around 53% in 2023. Rolls denote a continuous length of laminated label material wound around a cylindrical core. Rolls facilitate high-volume production, as they can accommodate a larger quantity of label material than sheets. This minimizes the need for frequent material changeovers during printing and manufacturing, enhancing production efficiency and reducing downtime. Moreover, utilizing rolls leads to reduced material waste. Continuous production enabled by rolls allows label manufacturers to optimize material usage, resulting in cost savings and improved sustainability. Rolls offer flexibility in label length, allowing manufacturers to cater to diverse customer requirements and application needs. This adaptability facilitates customization. These benefits offered by Rolls translate to its dominance in the global market.

The composition segment is divided into adhesive, facestock and release liner. The facestock segment dominated the market, with a market share of around 38% in 2023. The facestock composition in laminated labels refers to the layer of label material directly printed upon, which serves as the visible surface. It is crucial for laminated labels' performance, appearance, and durability. Facestocks are typically made from paper, film, or synthetic materials such as polyester, polypropylene, or polyethylene.

The printing technology segment is divided into digital, flexography, lithography, and others. The digital segment dominated the market, with a market share of around 40% in 2023. Digital printing technology is a method of printing where digital-based images are directly printed onto various substrates, such as paper, film, or synthetic materials, using inkjet or laser printers. Digital printing offers high-quality printing with vibrant colours, sharp images, and fine details, making it ideal for producing visually appealing labels. This high-quality printing capability enhances brand visibility and attracts consumer attention in competitive markets. Digital printing allows for customization and personalization of labels. Additionally, digital printing offers cost-effective short print runs and variable data printing solutions, eliminating the need for expensive setup costs and printing plates associated with traditional printing methods. Digital printing technology's combination of high-quality printing, customization capabilities, cost-effectiveness, and efficiency makes it the preferred choice for laminated labels in various industries.

The application segment is divided into food and beverages, manufacturing, fashion and apparel, electronics and appliances, pharmaceuticals, retail labels and others. The food and beverages segment dominated the market, with a market share of around 36% in 2023. Laminated labels are essential in the food and beverage industry, given the need to offer information according to governing regulations, brand differentiation, and marking needs, among other requirements. The industry's growth, propelled by population expansion, urbanization, and changing consumer preferences, positively impacts laminated label demand.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2023 | USD 80 Billion |

| Market size value in 2033 | USD 130.31 Billion |

| CAGR (2024 to 2033) | 5% |

| Historical data | 2020-2022 |

| Base Year | 2023 |

| Forecast | 2024-2033 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Material Type, Form, Composition, Printing Technology and Application |

As per The Brainy Insights, the size of the global laminated labels market was valued at USD 80 billion in 2023 to USD 130.31 billion by 2033.

Global laminated labels market is growing at a CAGR of 5% during the forecast period 2024-2033.

The market's growth will be influenced by the increasing demand for labelling solutions across diverse industries.

The cost of laminated labels could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global laminated labels market based on below mentioned segments:

Global Laminated labels Market by Material Type:

Global Laminated labels Market by Form:

Global Laminated labels Market by Composition:

Global Laminated labels Market by Printing Technology:

Global Laminated labels Market by Application:

Global Laminated labels Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date