- +1-315-215-1633

- sales@thebrainyinsights.com

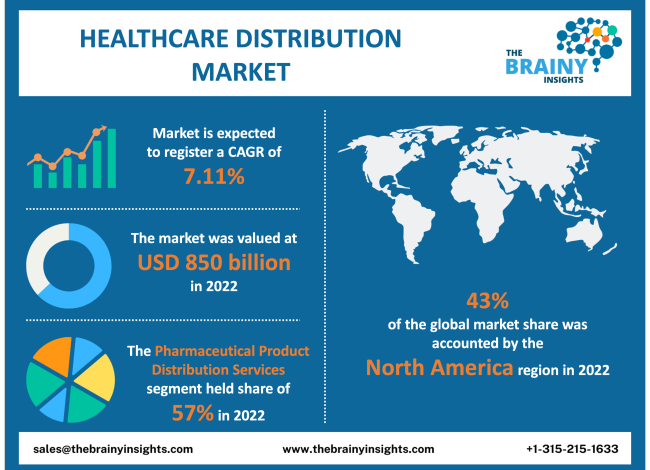

The global healthcare distribution market is expected to grow from USD 850 billion in 2022 to USD 1689.34 billion by 2032, at a CAGR of 7.11% during the forecast period 2023-2032. The increasing incidence of chronic and acute diseases will drive the global healthcare distribution market.

Good health or individual well-being is the absence of illness, diseases, or conditions, and it is a person's social, physical, and mental stability and wellness. However, sometimes the individual suffers deviations from their well-being state. An intervention is required to gain back wellness. Maintaining good habits and lifestyle to ensure physical, mental, and social well-being is also equally necessary. The function of maintaining individual and community health is the responsibility of the healthcare sector. They undertake measures to prevent, diagnose, and cure illnesses, injuries, and diseases. However, these healthcare services need to be delivered to the consumer through a robust network of distributors. Healthcare distribution is a system involving several stakeholders, processes, mechanisms, and logistics that are coherently connected to deliver healthcare services like medicines, medical devices, diagnostics, and treatments to consumers efficiently.

Get an overview of this study by requesting a free sample

January 2023 - Open Medical announced a new cooperation with Tamer Group to provide the Kingdom of Saudi Arabia with its award-winning, market-leading digital transformation solutions (KSA). Open Medical aspires to assist the KSA's forward-thinking innovators in their mission to reimagine the effectiveness and quality of healthcare. They aim to work with healthcare providers, payers, and medical device and pharmaceutical organizations to develop ground-breaking digital solutions along the whole transformation path. The best-in-class Open Medical platform, PathpointR, offers specialized digital transformation solutions that are intended to improve and streamline care throughout the healthcare ecosystem while lowering providers' costs and enabling clinicians to provide data-driven care for patients.

January 2023 - GulfDrug opened a brand-new cutting-edge supply chain, management, and training center in the Industrial City of Abu Dhabi (ICAD) to improve the strength and connectivity of its pharmaceutical and medical distribution and management across the nation. Senior managers, board members, and important industry participants and suppliers attended the event. The newest smart building with cutting-edge capabilities is proof of GulfDrug's dedication to more than 50 years of loyal service to the country.

The increasing demand for healthcare services – The contemporary world has witnessed drastic lifestyle changes that are detrimental to the population's physical, mental, and social well-being. For instance, the prevalent sedentary lifestyle associated with prolonged desk jobs, increased screen time, lack of physical exercise, unhealthy diet, and stressful work environment have contributed to rising chronic and acute health conditions. The increasing incidence and prevalence of cardiovascular, respiratory, auto-immune, ENT, and lifestyle diseases/conditions indicate the rising demand for healthcare services. Increasing accidents and traumas also contribute to the rising demand for medical care. The growing focus on mental health is also encouraging the expansion of healthcare services to cover a broader spectrum of human well-being. The ever-increasing demand for generic medicines facilitated by novel drug development by market players is also positively contributing to the market. The increasing disposable income of the population is increasing the patient market pool. Government initiatives aimed at ramping up healthcare infrastructure, devising and implementing federal healthcare initiatives, and favorable reimbursement policies are also supporting the market's growth. Therefore, the increasing incidence of multiple acute and chronic conditions will increase the demand for healthcare services due to changing lifestyles and environmental conditions. The growing demand for healthcare services, will in turn, encourage the authorities to ramp up healthcare infrastructure, including a robust healthcare distribution network of manufacturers, suppliers, distributors, and retailers, thereby driving the market's growth.

Pharmaceuticals are expensive – Pharmaceutical distribution services dominate healthcare distribution services. However, these services are often pricey at a retail market level. The lack of favorable government reimbursement policies in several countries also contributes to the rising inaccessibility of healthcare globally. The presence of significant market players and distributors is restricted to a specific global region, which impedes the general population's accessibility. The incomplete coverage of government healthcare initiatives leaves a significant portion of the population vulnerable to exploitation by big pharma. Therefore, the government's inability to provide for everyone in need leaves a market gap exploited by pharmaceuticals for profit-making. The expensive healthcare products and services limit the global healthcare distribution market's ability to achieve its full potential.

Improvement in logistical technologies and processes to improve supply chain resilience – Technology is advancing quickly across industries, and artificial intelligence, cloud computing, the internet of things, cyber-physical systems, and data analytics are becoming increasingly popular. Digitalization, automation, and cross-sector technology integration are vital components of industrialization 4.0. Population growth has boosted market consumer demand for pharmaceuticals, which must be met by raising industry production levels. By offering real-time asset management and improved operation control, new technologies like radio frequency identification technology (RFIT) may increase production efficiency in the pharmaceutical and healthcare sector while saving time and money. RFID ensures efficient resource usage, cutting overhead costs and boosting revenue. Radiofrequency identification technology (RFID) is used to speed up the delivery of high-quality items and offer automated inventory management. Real-time inventory data is provided by the sensors used to track objects. The straightforward layout takes up less room, which increases manufacturing effectiveness. The mentioned advantages allow healthcare distribution to expand efficiently while optimizing resources and offering lucrative opportunities in the forecast period.

High investment capital is required to set up a strong healthcare distribution network – Developing and setting up a robust healthcare distribution system requires several resources. It involves enormous capital investment and high maintenance costs. The large pool of stakeholders in the system also demands significant effort in terms of money, work, time, and intellect. All this is costly and might not be affordable for every economy worldwide. Middle- and low-income countries are especially cornered given their low financing ability to develop a healthcare distribution system. Excluding such a vast consumer market from the global healthcare distribution market will challenge its growth.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. The North American region emerged as the most significant global healthcare distribution market, with a 43% market revenue share in 2022. The increasing incidence and prevalence of cardiovascular, respiratory, ENT, and other chronic and acute diseases/conditions in the region are contributing to the rising demand for healthcare services. The region's well-established and funded pharmaceutical and healthcare sector is catering to this increasing demand. The growing presence of pharma chains with comprehensive network coverage of retail pharmacies facilitates the regional market's growth. Big pharmaceuticals and biotechnology companies contribute to the increasing research and development of advanced healthcare medicine, instruments, equipment, and devices. Access to high-tech machinery and technological advancements facilitates product innovation in the region. The high per capita income of the countries is complemented by favorable reimbursement policies offered by the government, driving up pharma sales and augmenting the regional market's growth. The rising government spending on ramping up healthcare distribution infrastructure after covid-19 pandemic with an aim towards achieving self-sufficiency and reducing dependency on China will also propel the regional market’s growth.

North America region Healthcare Distribution Market Share in 2022 - 43%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The product type segment is divided into pharmaceutical product distribution services, medical device distribution services, and biopharmaceutical distribution services. The pharmaceutical product distribution services segment dominated the market with a revenue share of around 57% in 2022. The increasing incidence of several chronic and acute diseases and conditions has increased the demand for pharmaceuticals to treat these diseases/conditions, alleviate their symptoms or manage them. The increasing disposable income of consumers has enabled users to access novel pharmaceuticals, augmenting their demand in the global market. The growing research and development to produce advanced and effective drugs have also contributed positively to the segment's market. The extensive network of pharmaceutical distributors also aids the segment's growth. The increasing presence of pharmaceuticals in the Asian market, especially after the covid-19 pandemic, will propel the segment's growth and development.

The end-user segment is divided into retail pharmacies, hospital pharmacies, physician offices, online pharmacies, home care settings, clinical laboratories, and others. The retail pharmacies segment dominated the market with a revenue share of around 47% in 2022. Retail pharmacies can be stand-alone or retail chains like Greenline and CVS. They are in direct contact with the consumers and cater to their prescription-based medicine demands and generic drugs daily. They are dispensers of the pharmaceuticals and medical devices like oximeters. They ensure last-mile delivery of medicine. The growing presence of retail pharmacies has contributed to the rising dominance of the segment in the global market. The increasing disposable income has also favored the segment's growth. The government also contributes to the segment's development by establishing public retail pharmacies and devising favorable prescription reimbursement policies. Therefore, the segment will continue to dominate the market with a positive push from the public authorities and private players and robust consumer demand.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2022 | USD 850 Billion |

| Market size value in 2032 | USD 1689.34 Billion |

| CAGR (2023 to 2032) | 7.11% |

| Historical data | 2019-2021 |

| Base Year | 2022 |

| Forecast | 2023-2032 |

| Regional Segments | The regions examined for the market are Europe, Asia Pacific, North America, South America, and Middle East & Africa. |

| Segments | The research segment is based on product type and end-user. |

As per The Brainy Insights, the size of the healthcare distribution market was valued at USD 850 billion in 2022 to USD 1689.34 billion by 2032.

Global healthcare distribution market is growing at a CAGR of 7.11% during the forecast period 2023-2032.

The market's growth will be influenced by the increasing demand for healthcare services.

Pharmaceuticals are expensive and that could hamper the market growth.

1. Introduction

1.1. Objectives of the Study

1.2. Market Definition

1.3. Research Scope

1.4. Currency

1.5. Key Target Audience

2. Research Methodology and Assumptions

3. Executive Summary

4. Premium Insights

4.1. Porter’s Five Forces Analysis

4.2. Value Chain Analysis

4.3. Top Investment Pockets

4.3.1. Market Attractiveness Analysis By Product Type

4.3.2. Market Attractiveness Analysis By End User

4.3.3. Market Attractiveness Analysis By Region

4.4. Industry Trends

5. Market Dynamics

5.1. Market Evaluation

5.2. Drivers

5.2.1. The increasing demand for healthcare services

5.3. Restraints

5.3.1. Pharmaceuticals are expensive

5.4. Opportunities

5.4.1. Improvement in logistical technologies and processes to improve supply chain resilience

5.5. Challenges

5.5.1. High investment capital is required to set-up strong healthcare distribution network

6. Global Healthcare Distribution Market Analysis and Forecast, By Product Type

6.1. Segment Overview

6.2. Pharmaceutical Product Distribution Services

6.3. Medical Device Distribution Services

6.4. Biopharmaceutical Distribution Services

7. Global Healthcare Distribution Market Analysis and Forecast, By End User

7.1. Segment Overview

7.2. Retail Pharmacies

7.3. Hospital Pharmacies

7.4. Physician Offices

7.5. Online Pharmacies

7.6. Home Care Settings

7.7. Clinical Laboratories

7.8. Others

8. Global Healthcare Distribution Market Analysis and Forecast, By Regional Analysis

8.1. Segment Overview

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.2.3. Mexico

8.3. Europe

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.4. Asia-Pacific

8.4.1. Japan

8.4.2. China

8.4.3. India

8.5. South America

8.5.1. Brazil

8.6. Middle East and Africa

8.6.1. UAE

8.6.2. South Africa

9. Global Healthcare Distribution Market-Competitive Landscape

9.1. Overview

9.2. Market Share of Key Players in the Healthcare Distribution Market

9.2.1. Global Company Market Share

9.2.2. North America Company Market Share

9.2.3. Europe Company Market Share

9.2.4. APAC Company Market Share

9.3. Competitive Situations and Trends

9.3.1. Product Launches and Developments

9.3.2. Partnerships, Collaborations, and Agreements

9.3.3. Mergers & Acquisitions

9.3.4. Expansions

10. Company Profiles

10.1. AmerisourceBergen Corporation

10.1.1. Business Overview

10.1.2. Company Snapshot

10.1.3. Company Market Share Analysis

10.1.4. Company Product Portfolio

10.1.5. Recent Developments

10.1.6. SWOT Analysis

10.2. Cardinal Health

10.2.1. Business Overview

10.2.2. Company Snapshot

10.2.3. Company Market Share Analysis

10.2.4. Company Product Portfolio

10.2.5. Recent Developments

10.2.6. SWOT Analysis

10.3. FFF Enterprises Inc.

10.3.1. Business Overview

10.3.2. Company Snapshot

10.3.3. Company Market Share Analysis

10.3.4. Company Product Portfolio

10.3.5. Recent Developments

10.3.6. SWOT Analysis

10.4. Henry Schein Inc.

10.4.1. Business Overview

10.4.2. Company Snapshot

10.4.3. Company Market Share Analysis

10.4.4. Company Product Portfolio

10.4.5. Recent Developments

10.4.6. SWOT Analysis

10.5. McKesson Corporation

10.5.1. Business Overview

10.5.2. Company Snapshot

10.5.3. Company Market Share Analysis

10.5.4. Company Product Portfolio

10.5.5. Recent Developments

10.5.6. SWOT Analysis

10.6. Medline Industries Inc.

10.6.1. Business Overview

10.6.2. Company Snapshot

10.6.3. Company Market Share Analysis

10.6.4. Company Product Portfolio

10.6.5. Recent Developments

10.6.6. SWOT Analysis

10.7. Morris and Dickson Co. LLC

10.7.1. Business Overview

10.7.2. Company Snapshot

10.7.3. Company Market Share Analysis

10.7.4. Company Product Portfolio

10.7.5. Recent Developments

10.7.6. SWOT Analysis

10.8. Owens & Minor Inc.

10.8.1. Business Overview

10.8.2. Company Snapshot

10.8.3. Company Market Share Analysis

10.8.4. Company Product Portfolio

10.8.5. Recent Developments

10.8.6. SWOT Analysis

10.9. Patterson Companies Inc.

10.9.1. Business Overview

10.9.2. Company Snapshot

10.9.3. Company Market Share Analysis

10.9.4. Company Product Portfolio

10.9.5. Recent Developments

10.9.6. SWOT Analysis

10.10. Rochester Drug Cooperative Inc.

10.10.1. Business Overview

10.10.2. Company Snapshot

10.10.3. Company Market Share Analysis

10.10.4. Company Component Portfolio

10.10.5. Recent Developments

10.10.6. SWOT Analysis

List of Table

1. Global Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

2. Global Pharmaceutical Product Distribution Services Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

3. Global Medical Device Distribution Services Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

4. Global Biopharmaceutical Distribution Services Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

5. Global Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

6. Global Retail Pharmacies Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

7. Global Hospital Pharmacies Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

8. Global Physician Offices Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

9. Global Online Pharmacies Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

10. Global Home Care Settings Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

11. Global Clinical Laboratories Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

12. Global Others Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

13. Global Healthcare Distribution Market, By Region, 2019-2032 (USD Billion)

14. North America Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

15. North America Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

16. U.S. Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

17. U.S. Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

18. Canada Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

19. Canada Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

20. Mexico Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

21. Mexico Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

22. Europe Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

23. Europe Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

24. Germany Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

25. Germany Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

26. France Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

27. France Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

28. U.K. Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

29. U.K. Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

30. Italy Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

31. Italy Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

32. Spain Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

33. Spain Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

34. Asia Pacific Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

35. Asia Pacific Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

36. Japan Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

37. Japan Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

38. China Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

39. China Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

40. India Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

41. India Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

42. South America Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

43. South America Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

44. Brazil Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

45. Brazil Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

46. Middle East and Africa Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

47. Middle East and Africa Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

48. UAE Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

49. UAE Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

50. South Africa Healthcare Distribution Market, By Product Type, 2019-2032 (USD Billion)

51. South Africa Healthcare Distribution Market, By End User, 2019-2032 (USD Billion)

List of Figures

1. Global Healthcare Distribution Market Segmentation

2. Healthcare Distribution Market: Research Methodology

3. Market Size Estimation Methodology: Bottom-Up Approach

4. Market Size Estimation Methodology: Top-Down Approach

5. Data Triangulation

6. Porter’s Five Forces Analysis

7. Value Chain Analysis

8. Global Healthcare Distribution Market Attractiveness Analysis By Product Type

9. Global Healthcare Distribution Market Attractiveness Analysis By End User

10. Global Healthcare Distribution Market Attractiveness Analysis By Region

11. Global Healthcare Distribution Market: Dynamics

12. Global Healthcare Distribution Market Share by Product Type (2022 & 2032)

13. Global Healthcare Distribution Market Share by End User (2022 & 2032)

14. Global Healthcare Distribution Market Share by Regions (2022 & 2032)

15. Global Healthcare Distribution Market Share by Company (2021)

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. The Brainy Insights has segmented the healthcare distribution market based on below mentioned segments:

Healthcare Distribution Market by Product Type:

Healthcare Distribution Market by End User:

Healthcare Distribution Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date