- +1-315-215-1633

- sales@thebrainyinsights.com

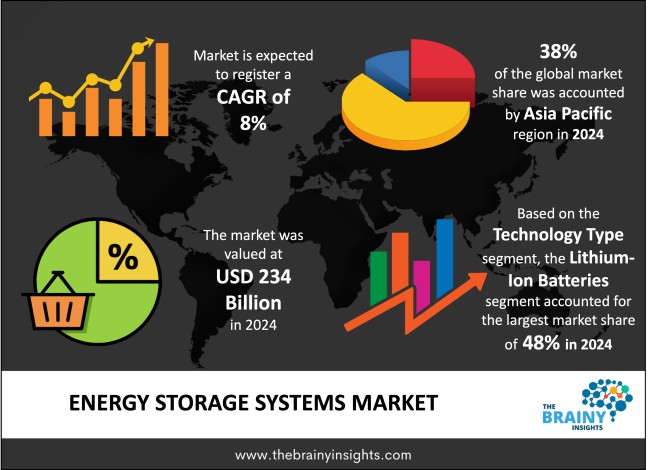

The global energy storage systems market was valued at USD 234 billion in 2024 and grew at a CAGR of 8% from 2025 to 2034. The market is expected to reach USD 505.18 billion by 2034. The increasing energy demands will drive the growth of the global energy storage systems market.

Energy storage systems (ESS) are technologies designed to collect the energy and store it until later use, which is beneficial in increasing the flexibility, reliability, and the efficiency of the energy supply systems. With the energy sector in the world moving towards the use of renewable energy, ESS has become the cornerstone of both the supply-demand balance. Such systems are used to store surplus of electricity when produced in abundance and discharge it when it is required because of high demand or low production thereby stabilization of the grid to enable continuity of the supply of power all times. Mechanical, thermal, chemical, and electrochemical are bracketed in energy storage and some typical storage methods would be mechanical storage, thermal storage, chemical storage and electrochemical storage. Lithium-ion batteries are the most predominant among them because of their energy density, efficiency and significantly declining expenses. ESS find application in a myriad of products and systems, which include grid-scale energy storage and renewable energy integration, backup power systems and longer-term residential systems. Both governments and the private sectors are investing in ESS heavily in order to achieve climate targets, aiding decarbonization and enhancing grid resilience. Additional system capabilities are being brought by technological developments to include solid-state batteries, AI-enabled energy management systems and second-life batteries. The energy storage industry is an industry that is fast developing despite the obstacles such as high start-up costs, resource shortage, and safety measures. Simply put, energy storage systems are turning out to be the spine of contemporary, green energy infrastructure making a painless shift to low-carbon economies and a more intelligent grid possible.

Get an overview of this study by requesting a free sample

Technological advancements – The ongoing advances in battery technologies, most importantly, the lithium-ion and other new innovations such as solid-state and flow batteries will drive the market’s growth. The resulting ESS energy densities are greater, charging rates are quicker, life spans are longer, and they are safer and thus systems based on ESS are more applicable in various applications. There has also been an improvement of the manufacturing process and economies of scale leading to an extremely low-cost production of components of the battery which include lithium, cobalt, and nickel. Connection with intelligence systems including artificial intelligence (AI), the Internet of Things (IoT), and an energy management software in the cloud, has borne efficiency in the performance they offer to system and the responsiveness in the real world. This enables predictive maintenance, reduced energy consumption, improved connections with smart grids as well as distributed energy resources. In addition, scalability has been made possible through the customization of products and modular design with manufacturers able to accommodate residential, commercial and grid-scale customers with bespoke programs. There has also been an enhanced safety, improving thermal management systems, fireproofing material, and safe battery chemistries, making them more confident using it. All these developments have increased the reliability, efficiency and flexibility of ESS thereby rendering it more competitive as an investment to a variety of stakeholders.

Technical, financial and operational limitations – A large upfront cost can be characterized as one of the biggest barriers when it comes to energy storage systems market, as the cost includes the cost of batteries, inverters, cost of installation, as well as, integration with the existing infrastructure. This expenditure is especially limiting to both small scale or residential users where there is no apparent return on investment. Moreover, the performance of energy storage technologies such as lithium-ion batteries can experience degradation due to the loss of its capacity and efficiency, and this, as well, poses a negative effect on long-term performance and value. Issues in safety also exist, such that high-energy-density batteries are potentially at risk of thermal runaway or fire risk, raising concern in reliability and liability. The excessive reliance on the vital raw materials like lithium, cobalt, and nickel is another constraint that does not only increase total production costs but also predisposes the supply chain to geophysical and ethical concerns. Failure to achieve standardisation in the design of systems and communication protocols integrates leads to interoperability issues. Lastly, there is the issue of end-of life management of batteries, as not enough recycling infrastructure exists and there are no obvious regulations over their disposal, which creates both environmental and cost concerns.

Supportive regulatory framework – The world governments are already putting supportive policies in place to boost the use of ESS, including tax incentives, renewable integration requirement, net metering and storage-specific goals. The interest in grid modernization and energy storage is further being driven by climate change concerns and net-zero commitments as nations seek to decarbonize their energy apparatus by the end of this decade. In addition, rising cases of grid reliability, power cuts, natural catastrophes are lucrative as there is a demand in backup energy sources and grid reliability a list that ESS satisfy. Energy demand is also increasing due to the outright electrification of the transportation and industrial systems, and storage is needed to store energy when peak and increase the existing vehicle charging infrastructure and stabilize industrial power consumption. Moreover, storage systems are especially providing guard against geopolitical risks in energy security, supply interruptions, and energy prices that are travelling unpredictably. Residential and commercial demand in ESS is being propelled by the growing popularity of decentralized systems in energy production.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific emerged as the most significant global energy storage systems market, with a 38% market revenue share in 2024.

Most countries are at the forefront in ensuring energy integration and energy security through renewable energy resources and these nations include China, India, Japan, South Korea and Australia who are notably investing a lot in renewable energy. China is especially dominant, given that it is the greatest manufacturer and consumer of energy storage technologies and that it is the world leading lithium-ion battery producer. Its ambitious renewable energy mandates, together with supportive policies and subsidies on utility-scale ESS, have led to massive deployments of utility-scale ESS. India is also turning out to be a major figure with its ambitions of achieving 500 GW of non-fossil power by 2030. In the meantime, Japan and South Korea are using ESS to develop disaster resilience and smart grid and making heavy investments in residential and commercial storage. The location also has a strong supply chain due to the presence of a strong manufacturing ecosystem in the region, particularly battery manufacturing, which so far contributes to cost competitiveness and supply chain of the battery manufacturing industry. The market growth has also increased with government programs like subsidies, tax breaks and storage requirements. As Asia Pacific develops and energy demand is projected to reach an all-time high due to population growth and urbanization and the aging of its population in the future, it is projected to remain the global leader in the installation of ESS systems.

Asia Pacific Region Energy Storage Systems Market Share in 2024 - 38%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The technology type segment is divided into lithium-ion batteries, lead-acid batteries, flow batteries, sodium-based batteries, flywheels, compressed air energy storage (CAES) and pumped hydro storage. The lithium-ion batteries segment dominated the market, with a market share of around 48% in 2024. The global energy storage systems (ESS) market is driven by the lithium-ion batteries because of their outstanding performance features, scalability, and the falling prices. The batteries have a high energy density, so they are particularly suitable both to stationary and mobile applications. The fact that they have high round-trip efficiencies also means that they do not lose much energy during charging or discharging cycles and that feature is important in cases of grid balancing, peak shaving, and renewable integration. It also supports fast response time and high cycling stability of batteries which means that the lithium-ion batteries can also be used to control frequencies and frequency regulation amongst other ancillary services. They can flexibly be deployed in both residential and commercial projects and utility scale projects because of their modularity and flexible deployment options. Additionally, well-established supply chain structure and supplier ecosystem have helped in the further spread and adoption of the technology. Altogether, lithium-ion battery systems due to their performance level, cost-effectiveness, and technological maturity remain to be the most popular and leading battery system on the entire market of energy storage systems in the world.

The application segment is divided into electricity grid management, renewable integration, backup power, peak shaving, load shifting, ancillary services and microgrids. The electricity grid management segment dominated the market, with a market share of around 38% in 2024. The electricity grid management constitutes the largest application segment of the global energy storage systems (ESS) market as more electricity is required to operate together with flexibility, resilience, and stability with more prevalence of renewable energy. ESS can help in supporting critical grid services, including frequency regulation, voltage control, and load balancing, thus helping utilities to maximize their operations due to the delay in upgrading their infrastructure. Furthermore, storage of energy enables time-shifting of electricity, which reduces peak demand more effectively. As more sectors get electrified and the energy generation becomes decentralized due to distributed generation, grid operators increasingly have to deal with more complicated demand-supply interaction. In this regard, ESS can provide a support of grid in real time, as well as grant an improvement upon the flexibility of grid. ESS deployment on electricity grid applications has also been speeded up by regulatory changes and government requirements in a number of territories.

The end-use industry segment is divided into utility, commercial & industrial and residential. The utility segment dominated the market, with a market share of around 55% in 2024. The largest end-use of the global market of energy storage systems (ESS), namely, utilities, is associated both with their most strategic position in the production, transmission, and distribution of energy, and with the fact that utilities may invest in large-scale infrastructures. With a shifting energy mix toward renewables in the world, utilities have the task of accommodating such variable generation sources, such as solar and wind, into their grid and maintaining stability and reliability in the supply of electricity. Storing energy presents a practical solution as a utility can store surplus when demand is low or generation high and then release it when demand is high or when sun and wind are not where they should be. This role is essential when it comes to grid stability and control of their frequency, which is becoming more and more pertinent as the proportion of renewables increases. ESS can also be used by utilities to postpone or even to avoid the necessity of a more expensive upgrade to old transmission and distribution infrastructure, as storage will be used to mitigate congestion and transmission losses, and improve system flexibility.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 234 Billion |

| Market size value in 2034 | USD 505.18 Billion |

| CAGR (2025 to 2034) | 8% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Technology Type, Application and End-Use Industry |

As per The Brainy Insights, the size of the global energy storage systems market was valued at USD 234 billion in 2024 to USD 505.18 billion by 2034.

Global energy storage systems market is growing at a CAGR of 8% during the forecast period 2025-2034.

The market's growth will be influenced by technological advancements.

Technical, financial and operational limitations could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global energy storage systems market based on below mentioned segments:

Global Energy Storage Systems Market by Technology Type:

Global Energy Storage Systems Market by Application:

Global Energy Storage Systems Market by End-Use Industry:

Global Energy Storage Systems Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date