- +1-315-215-1633

- sales@thebrainyinsights.com

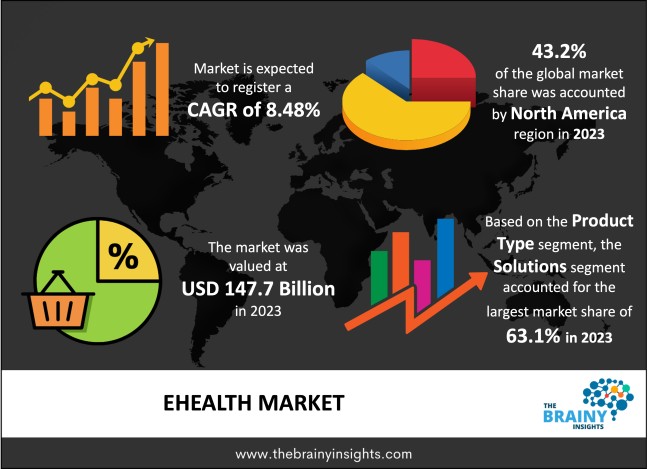

The global eHealth market was valued at USD 147.7 billion in 2023 and grew at a CAGR of 8.48% from 2024 to 2033. The market is expected to reach USD 333.33 billion by 2033. The increasing demand for digital healthcare management systems will drive the growth of the global eHealth market. The increasing use of patient-focused, digital care technologies is a major force behind expanding the global eHealth market. This growth is fuelled primarily by hospitals and patients' growing interest in digitally-based healthcare products and services digitally based. E-health platforms have rapidly drawn widespread attention worldwide due to their ease of accessibility for health professionals around-the-clock, driving demand for services like consultation and education. Additionally, the rising adoption of smart devices and the increased number of smartphone users have fostered growth within this sector globally.

According to the WHO, the cost-effective and secure application of information and communication technology in support of health and health-related sectors is known as eHealth. eHealth integrates IT with health care services, surveillance, education, knowledge, and research. With simple, quick, and easy access to patient information, eHealth is a great tool for storing patient data and assisting doctors in making better decisions. The capacity to manage personal data gives patients security and gives them control over its transfer and shareability. Users of eHealth can also communicate with other people or their doctors using text, voice, video, and other sorts of data. It can create reminders for taking medications and tests and plan remote monitoring appointments and routine exams. Time is saved, and efficiency is increased with eHealth. Additionally, it raises health consciousness, which over time lessens the burden of disease. Administrative load is lessened via eHealth. It can halt unnecessary interventions or diagnoses by improving communication among healthcare organisations. E-health can potentially reduce costs for regulatory agencies, patients, and healthcare providers.

Get an overview of this study by requesting a free sample

The increasing demand for digital healthcare management systems – the covid-19 pandemic highlighted the inadequacies in the national healthcare systems of even the most developed countries. The lack of hospital beds, medicines, vaccines etc., led to millions of preventable deaths. The failure of healthcare systems prompted the fiscal authorities and other stakeholders to facilitate reforms to improve the healthcare infrastructure and the overall ecosystem to meet the rising healthcare demands. Automation and digitization are revolutionizing healthcare to improve efficiency and patient outcomes and meet the goal of timely and universal healthcare for all. Digital healthcare systems are being deployed to consolidate, streamline and standardise the healthcare system. For instance, Digital tools give professionals a more comprehensive view of patient health and give individuals greater control over their health. Digital healthcare management systems have helped Healthcare organisations improve worker satisfaction and patient care and enable better and quicker diagnostics by implementing cutting-edge tech solutions. It also enables expanding healthcare solutions to reach the last mile. It reduces costs for patients and providers. Therefore, the increasing demand and adoption of digital healthcare management systems will bode well for the market's growth.

The lack of infrastructure – underdeveloped and developing nations lack the IT infrastructure to expand the eHealth market. The low internet penetration or poor-quality data connectivity has stalled eHealth adoption. The lack of data literacy in these nations also contributes to the market's limited growth. Additionally, the structural complications with the dearth of qualified professionals to operate the eHealth components are hampering the market's growth.

The introduction of AI, IoT and 5G technologies – the industry 4.0 decade is associated with using technology to automate and digitize the economy. The same is being witnessed in the healthcare industry. The healthcare industry has an unexploited potential that has encouraged market players to invest money in technological advancements and product innovations that can be employed against lucrative prospects. Concepts like data analytics, cloud computing, the Internet of Things, and artificial intelligence are becoming increasingly common as technology develops quickly. It is possible that the adoption of these cutting-edge technologies in the healthcare sector would revolutionise the field and increase productivity, efficiency, and patient outcomes. It will lower costs and meet the expanding demand for healthcare. AI technologies may assist healthcare organisations in making the most of their data, resources, and assets by analysing data patterns, which increases efficiency and enhances the performance of clinical and operational workflows, processes, and financial operations. Therefore, during the forecast period, the technical developments in AI, AR, big data, IoT, and cyber-security will all impact the market's growth and development.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the largest global eHealth market, with a 43.2% market revenue share in 2023.

The well-established and mature IT industry with the necessary infrastructure offering high-speed internet to the users in the region is driving the market's growth. The increasing awareness about eHealth and the promotion of the same by the significant number of market players present in the region will bode well for the market. Several surveys have concluded the adoption of eHealth applications by residents of the US and Canada, given the convenience and ease it offers.

North America Region eHealth Market Share in 2023 – 43.2%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The product type segment is divided into services and solutions. The solutions segment dominated the market, with a market share of 63.1% in 2023. The eHealth solutions contain a variety of options, each defined for a particular object. It includes Electronic Health Records, which acquire patient data, store and transfer it with patient consent whenever required and streamline diagnosis and treatment. Radiology information systems, Vendor Neutral Archive (VNA) picture archiving and & Communications Systems(PACS), and Laboratory Information Systems (LIS) help consolidate findings in the diagnosis stage, thereby improving patient outcomes. Pharmacy information systems improve ease, convenience and access to medicine for users. Medical Apps facilitate virtual consultation and reduce hospitalization rates with timely interventions. eHealth solutions save time and money, improve efficiency and patient outcomes, reduce administrative burden and facilitate innovation. It improves health awareness and improves the overall community health. The presence of significant market players offering these solutions as third-party service providers, along with their expertise and round-the-clock maintenance, has driven the segment's growth.

The deployment type segment is divided into cloud and on-premises. The cloud segment dominated the market, with a market share of 68.2% in 2023. The cloud is accessible over the Internet. It can be remotely accessed and offers access control with the highest safety and security technologies deployed within the system. The network is a distributed group of servers. Cloud is scalable, flexible and reliable. It is cost-effective, which is the primary reason driving its dominance in the market. The system cannot be physically damaged and can be accessed and operated even during emergencies restricting physical access to healthcare spaces. Cloud optimizes space. Data backup and customizable features can improve resource allocation.

The end-user segment is divided into healthcare providers, patients, health insurance providers, pharmaceutical companies, app companies and others. The healthcare providers segment dominated the market, with a market share of 40.4% in 2023. The automation and digitization of the healthcare sector are growing. Both public and commercial players are utilising technology's promise for the healthcare sector. Healthcare providers use wearables, gadgets, and medical applications in various contexts to accomplish various goals. It is utilised to improve efficiency, service delivery, cut downtime, and streamline administration. It gathers, processes, maintains, and preserves health records to make patient care and policymaking easier to access. It also enhances departmental collaboration and cooperation To improve patient outcomes. Additionally, they are using it to educate and raise awareness.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2023 | USD 147.7 Billion |

| Market size value in 2033 | USD 333.33 Billion |

| CAGR (2024 to 2033) | 8.48% |

| Historical data | 2020-2022 |

| Base Year | 2023 |

| Forecast | 2024-2033 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East & Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Product Type, Deployment Type and End User |

As per The Brainy Insights, the size of the global eHealth market was valued at USD 147.7 billion in 2023 to USD 333.33 billion by 2033.

Global eHealth market is growing at a CAGR of 8.48% during the forecast period 2024-2033.

The market's growth will be influenced by the increasing demand for digital healthcare managements systems.

The lack of infrastructure could hamper the market growth.

1. Introduction

1.1. Objectives of the Study

1.2. Market Definition

1.3. Research Scope

1.4. Currency

1.5. Key Target Audience

2. Research Methodology and Assumptions

3. Executive Summary

4. Premium Insights

4.1. Porter’s Five Forces Analysis

4.2. Value Chain Analysis

4.3. Top Investment Pockets

4.3.1. Market Attractiveness Analysis by Product Type

4.3.2. Market Attractiveness Analysis by Deployment Type

4.3.3. Market Attractiveness Analysis by End User

4.3.4. Market Attractiveness Analysis by Region

4.4. Industry Trends

5. Market Dynamics

5.1. Market Evaluation

5.2. Drivers

5.2.1. The increasing demand for digital healthcare management apps

5.3. Restraints

5.3.1. The lack of infrastructure

5.4. Opportunities

5.4.1. The introduction of AI, IoT and 5G technologies

5.5. Challenges

5.5.1. The lack of data privacy rules and regulations

6. Global eHealth Market Analysis and Forecast, By Product Type

6.1. Segment Overview

6.2. Services

6.3. Solutions

7. Global eHealth Market Analysis and Forecast, By Deployment Type

7.1. Segment Overview

7.2. Cloud

7.3. On-Premises

8. Global eHealth Market Analysis and Forecast, By End User

8.1. Segment Overview

8.2. Healthcare Providers

8.3. Patients

8.4. Health Insurance Providers

8.5. Pharmaceuticals Companies

8.6. App Companies

8.7. Others

9. Global eHealth Market Analysis and Forecast, By Regional Analysis

9.1. Segment Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.2.3. Mexico

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.4. Asia-Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.5. South America

9.5.1. Brazil

9.6. Middle East and Africa

9.6.1. UAE

9.6.2. South Africa

10. Global eHealth Market-Competitive Landscape

10.1. Overview

10.2. Market Share of Key Players in the eHealth Market

10.2.1. Global Company Market Share

10.2.2. North America Company Market Share

10.2.3. Europe Company Market Share

10.2.4. APAC Company Market Share

10.3. Competitive Situations and Trends

10.3.1. Product Launches and Developments

10.3.2. Partnerships, Collaborations, and Agreements

10.3.3. Mergers & Acquisitions

10.3.4. Expansions

11. Company Profiles

11.1. Allscripts Healthcare Solutions, Inc

11.1.1. Business Overview

11.1.2. Company Snapshot

11.1.3. Company Market Share Analysis

11.1.4. Company Product Portfolio

11.1.5. Recent Developments

11.1.6. SWOT Analysis

11.2. Athenahealth, Inc,

11.2.1. Business Overview

11.2.2. Company Snapshot

11.2.3. Company Market Share Analysis

11.2.4. Company Product Portfolio

11.2.5. Recent Developments

11.2.6. SWOT Analysis

11.3. Cisco Systems Inc

11.3.1. Business Overview

11.3.2. Company Snapshot

11.3.3. Company Market Share Analysis

11.3.4. Company Product Portfolio

11.3.5. Recent Developments

11.3.6. SWOT Analysis

11.4. International Business Management Corporation

11.4.1. Business Overview

11.4.2. Company Snapshot

11.4.3. Company Market Share Analysis

11.4.4. Company Product Portfolio

11.4.5. Recent Developments

11.4.6. SWOT Analysis

11.5. Koninklijke Philips N.V

11.5.1. Business Overview

11.5.2. Company Snapshot

11.5.3. Company Market Share Analysis

11.5.4. Company Product Portfolio

11.5.5. Recent Developments

11.5.6. SWOT Analysis

11.6. Medtronic Plc

11.6.1. Business Overview

11.6.2. Company Snapshot

11.6.3. Company Market Share Analysis

11.6.4. Company Product Portfolio

11.6.5. Recent Developments

11.6.6. SWOT Analysis

11.7. Motion Computing Inc.

11.7.1. Business Overview

11.7.2. Company Snapshot

11.7.3. Company Market Share Analysis

11.7.4. Company Product Portfolio

11.7.5. Recent Developments

11.7.6. SWOT Analysis

11.8. Siemens AG

11.8.1. Business Overview

11.8.2. Company Snapshot

11.8.3. Company Market Share Analysis

11.8.4. Company Product Portfolio

11.8.5. Recent Developments

11.8.6. SWOT Analysis

11.9. Teladoc Health, Inc.

11.9.1. Business Overview

11.9.2. Company Snapshot

11.9.3. Company Market Share Analysis

11.9.4. Company Product Portfolio

11.9.5. Recent Developments

11.9.6. SWOT Analysis

11.10. UnitedHealth Group Inc.

11.10.1. Business Overview

11.10.2. Company Snapshot

11.10.3. Company Market Share Analysis

11.10.4. Company Product Portfolio

11.10.5. Recent Developments

11.10.6. SWOT Analysis

List of Table

1. Global eHealth Market, By Product Type, 2020-2033 (USD Billion)

2. Global Services eHealth Market, By Region, 2020-2033 (USD Billion)

3. Global Solutions eHealth Market, By Region, 2020-2033 (USD Billion)

4. Global eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

5. Global Cloud eHealth Market, By Region, 2020-2033 (USD Billion)

6. Global On-Premises eHealth Market, By Region, 2020-2033 (USD Billion)

7. Global eHealth Market, By End User, 2020-2033 (USD Billion)

8. Global Healthcare Providers eHealth Market, By Region, 2020-2033 (USD Billion)

9. Global Patients eHealth Market, By Region, 2020-2033 (USD Billion)

10. Global Health Insurance Providers eHealth Market, By Region, 2020-2033 (USD Billion)

11. Global Pharmaceuticals Companies eHealth Market, By Region, 2020-2033 (USD Billion)

12. Global App Companies eHealth Market, By Region, 2020-2033 (USD Billion)

13. Global Others eHealth Market, By Region, 2020-2033 (USD Billion)

14. Global eHealth Market, By Region, 2020-2033 (USD Billion)

15. North America eHealth Market, By Product Type, 2020-2033 (USD Billion)

16. North America eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

17. North America eHealth Market, By End User, 2020-2033 (USD Billion)

18. U.S. eHealth Market, By Product Type, 2020-2033 (USD Billion)

19. U.S. eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

20. U.S. eHealth Market, By End User, 2020-2033 (USD Billion)

21. Canada eHealth Market, By Product Type, 2020-2033 (USD Billion)

22. Canada eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

23. Canada eHealth Market, By End User, 2020-2033 (USD Billion)

24. Mexico eHealth Market, By Product Type, 2020-2033 (USD Billion)

25. Mexico eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

26. Mexico eHealth Market, By End User, 2020-2033 (USD Billion)

27. Europe eHealth Market, By Product Type, 2020-2033 (USD Billion)

28. Europe eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

29. Europe eHealth Market, By End User, 2020-2033 (USD Billion)

30. Germany eHealth Market, By Product Type, 2020-2033 (USD Billion)

31. Germany eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

32. Germany eHealth Market, By End User, 2020-2033 (USD Billion)

33. France eHealth Market, By Product Type, 2020-2033 (USD Billion)

34. France eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

35. France eHealth Market, By End User, 2020-2033 (USD Billion)

36. U.K. eHealth Market, By Product Type, 2020-2033 (USD Billion)

37. U.K. eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

38. U.K. eHealth Market, By End User, 2020-2033 (USD Billion)

39. Italy eHealth Market, By Product Type, 2020-2033 (USD Billion)

40. Italy eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

41. Italy eHealth Market, By End User, 2020-2033 (USD Billion)

42. Spain eHealth Market, By Product Type, 2020-2033 (USD Billion)

43. Spain eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

44. Spain eHealth Market, By End User, 2020-2033 (USD Billion)

45. Asia Pacific eHealth Market, By Product Type, 2020-2033 (USD Billion)

46. Asia Pacific eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

47. Asia Pacific eHealth Market, By End User, 2020-2033 (USD Billion)

48. Japan eHealth Market, By Product Type, 2020-2033 (USD Billion)

49. Japan eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

50. Japan eHealth Market, By End User, 2020-2033 (USD Billion)

51. China eHealth Market, By Product Type, 2020-2033 (USD Billion)

52. China eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

53. China eHealth Market, By End User, 2020-2033 (USD Billion)

54. India eHealth Market, By Product Type, 2020-2033 (USD Billion)

55. India eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

56. India eHealth Market, By End User, 2020-2033 (USD Billion)

57. South America eHealth Market, By Product Type, 2020-2033 (USD Billion)

58. South America eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

59. South America eHealth Market, By End User, 2020-2033 (USD Billion)

60. Brazil eHealth Market, By Product Type, 2020-2033 (USD Billion)

61. Brazil eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

62. Brazil eHealth Market, By End User, 2020-2033 (USD Billion)

63. Middle East and Africa eHealth Market, By Product Type, 2020-2033 (USD Billion)

64. Middle East and Africa eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

65. Middle East and Africa eHealth Market, By End User, 2020-2033 (USD Billion)

66. UAE eHealth Market, By Product Type, 2020-2033 (USD Billion)

67. UAE eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

68. UAE eHealth Market, By End User, 2020-2033 (USD Billion)

69. South Africa eHealth Market, By Product Type, 2020-2033 (USD Billion)

70. South Africa eHealth Market, By Deployment Type, 2020-2033 (USD Billion)

71. South Africa eHealth Market, By End User, 2020-2033 (USD Billion)

List of Figures

1. Global eHealth Market Segmentation

2. eHealth Market: Research Methodology

3. Market Size Estimation Methodology: Bottom-Up Approach

4. Market Size Estimation Methodology: Top-Down Approach

5. Data Triangulation

6. Porter’s Five Forces Analysis

7. Value Chain Analysis

8. Global eHealth Market Attractiveness Analysis by Product Type

9. Global eHealth Market Attractiveness Analysis by Deployment Type

10. Global eHealth Market Attractiveness Analysis by End User

11. Global eHealth Market Attractiveness Analysis by Region

12. Global eHealth Market: Dynamics

13. Global eHealth Market Share by Product Type (2023 & 2033)

14. Global eHealth Market Share by Deployment Type (2023 & 2033)

15. Global eHealth Market Share by End User (2023 & 2033)

16. Global eHealth Market Share by Regions (2023 & 2033)

17. Global eHealth Market Share by Company (2023)

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. The Brainy Insights has segmented the global eHealth market based on below mentioned segments:

Global eHealth Market by Product Type:

Global eHealth Market by Deployment Type:

Global eHealth Market by End User:

Global eHealth Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date