- +1-315-215-1633

- sales@thebrainyinsights.com

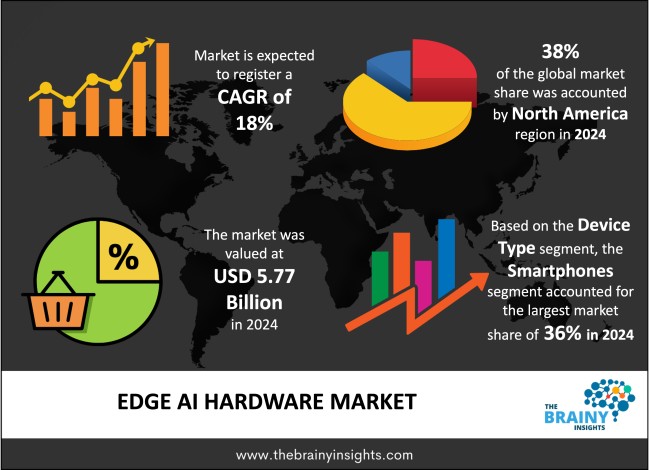

The global edge AI hardware market was valued at USD 5.77 billion in 2024 and grew at a CAGR of 18% from 2025 to 2034. The market is expected to reach USD 30.19 billion by 2034. The increasing healthcare expenditure will drive the growth of the global edge AI hardware market.

Edge AI hardware is made up of computers that locally process AI algorithms very close to where the data is produced, as opposed to sending the information to cloud servers. The analysed data can now be used and acted on quickly which improves privacy, makes latency shorter and requires less data transmission. Edge AI hardware is important in cases when fast decisions are needed, for example, in autonomous vehicles, smart cameras, industrial automation, healthcare devices and IoT applications. The key feature of edge AI hardware is a selection of components that make AI tasks run effectively even in small spaces. Such accelerators are Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), Field Programmable Gate Arrays (FPGAs), Application-Specific Integrated Circuits (ASICs) and Neural Processing Units (NPUs). Moreover, edge AI hardware is often equipped with memory, different types of sensors, Wi-Fi, 5G, Bluetooth and even embedded software for smooth deployment of AI models. Incorporating AI at the edge overcomes the main issues in regular cloud AI such as slow data processing speeds, high expenses and issues with privacy.

Get an overview of this study by requesting a free sample

Technological advancements and other similar improvements – the factors driving the demand for edge AI hardware are new and improved hardware products. The quick progress in semiconductor technology resulted in the creation of AI processors including Neural Processing Units (NPUs), Tensor Processing Units (TPUs), Application-Specific Integrated Circuits (ASICs) and Field Programmable Gate Arrays (FPGAs). With these chips, AI models can be used on edge devices with limited resources since they have the ability to deliver fast processing without wasting energy. The progress of AI algorithms has been important in addition to new hardware. Light AI models allow modern machine learning and deep learning to run now directly on computing devices without needing big servers for support. More importantly, power usage and reducing the size of electronics are now essential in designing devices. All in all, enhancing technology within the devices and creating new designs are key reasons why more edge AI hardware is in demand now.

High costs of production – A big problem with edge AI is that making and using specialized chips and devices costs a lot of money. Developing processors that are new to the market, like NPUs or TPUs, is expensive because it needs investment in research, development and production. Many small and medium-sized companies might shy away from edge AI, since its price is too high. Another main issue is how to keep edge devices operating with proper power and temperature while working close to the source of data. In addition, it is usually challenging and expensive to combine edge AI hardware with established IT systems, sensors and software platforms. Integrating several systems can make things slower and more expensive for companies which discourages more people from adopting technology. Even though edge AI hardware is close to the data, it is still unable to process much data due to its limited capabilities when compared to cloud services.

The increasing presence of IoT devices, autonomous vehicles, and other similar technologies and products – the increasing need for real-time data processes in areas such as self-driving cars, urban management, automation in factories and healthcare augments the market’s growth. Since such situations call for fast analysis and action that cloud systems cannot always give because of delays and connection problems, it is important to process AI locally on edge devices. Also, more focus on privacy and new regulations mean that organizations choose to store sensitive data nearby which increases the need for edge hardware to keep it secure. The rising number of IoT devices everywhere is important in increasing demand. Edge AI hardware allows data to be processed fast on the device, lowering the need for sending it via the internet and storing it online. Also, limited internet access in certain areas leads to the use of edge AI for making sure AI systems can operate reliably. It’s also vital to look at how effective a company is in terms of cost management. Decreasing the use of cloud services means businesses can reduce expenses on transferring and storing data. In addition, when it comes to the automotive, healthcare, retail and manufacturing sectors, the use of smart devices with edge AI helps them perform better and work independently. To sum up, these market conditions push the acceptance and growth of edge AI hardware everywhere.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global edge AI hardware market, with a 38% market revenue share in 2024.

The lead in edge AI hardware globally belongs to North America because of its powerful technology base, early adoption of new technologies and important players in the industry. Some of the biggest tech companies in the world such as Apple, Google, Intel, NVIDIA, AMD and Qualcomm, all located in the region, are pioneering hardware for AI. Investing much money in research and development, these firms help edge AI chips and devices to continue getting smarter. In addition, the area has developed a solid semiconductor network, powerful manufacturing base and good venture capital which promote fast commercial adoption of new AI technologies. The area’s success is driven by the fast take-up of AI in major industries, for example, consumer electronics, automotive, healthcare and industrial automation. Also, support from the government in the form of favorable policies and funds has been important for the region’s leadership in the field. Security and privacy policies in the United States have added to the development of edge AI by making data processing on devices the preferred approach to protect from cyber-attacks and keep up with regulations.

North America Region Edge AI Hardware Market Share in 2024 - 38%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The component segment is divided into processor, memory, sensor and others. The processor segment dominated the market, with a market share of around 38% in 2024. As the central part of edge AI systems, processors perform the AI functions such as machine learning, recognition of images and speech and working with natural language. On the other hand, running edge AI processing requires using Graphics Processing Units (GPUs), Neural Processing Units (NPUs), Tensor Processing Units (TPUs), Application-Specific Integrated Circuits (ASICs) and Field Programmable Gate Arrays (FPGAs) because they can handle the workload efficiently even though the devices are small and do not require much energy. Moreover, as AI features are included in consumer electronics, the demand for leading edge processors has increased. Semiconductor companies are spending a lot on AI chips that enable devices to handle AI tasks on their own, making devices faster, more reactive and better protected for users. On the whole, the processor’s important part in handling real-time AI with efficiency means it is the most significant component in AI hardware.

The device type segment is divided into smartphones, surveillance cameras, industrial robots, smart speakers, wearables, autonomous vehicles and edge servers. The smartphones segment dominated the market, with a market share of around 36% in 2024. Since billions of people own smartphones, they are considered the easiest and most common edge device which means AI can be rolled out on smartphones in large numbers. In today’s market, smartphones are fitted with powerful processors and specialized AI accelerators called Neural Processing Units (NPUs), allowing users to do tasks like facial recognition, use voice assistants, enhance pictures, translate languages, try augmented reality or input text in real time, all without using the cloud. Smartphone producers are using powerful edge AI chipsets because more people are demanding smartphone features that rely on AI. In addition, the influence of tech brands like Apple, Samsung, Qualcomm and Huawei on the smartphone world boosts the main use of edge AI components. They keep upgrading their AI-focused hardware to serve a variety of applications which range from tracking health to developing computational photography. As mobile AI lives up to new demands and what users seek, smartphones are the main focus for edge AI on devices. Their ability to be used everywhere, update their processors often and introduce new things are what make them number one in the market.

The power consumption segment is divided into less than 1W, 1–3W, 3–5W and more than 5W. The less than 1W segment dominated the market, with a market share of around 43% in 2024. A key factor for the top position of “less than 1W” in global edge AI hardware is it working well in devices that run on batteries and are small such as wearables, sensors and portable IoT gadgets. These gadgets need to run efficiently as energy is crucial and interruptions to power may happen. That is why many people choose components that draw less than 1 watt, as this lets the device function for longer periods without needing extra batteries or frequent charging. Such behaviour is crucial in remote medicine, smart farms and smart factories because remote equipment function without assistance for a long time. Since microcontrollers and energy-efficient NPUs with AI have appeared in the market, demand for sub-1W AI systems has gone up. They are created to handle particular AI tasks such as detecting anomalies, taking voice commands and conducting primitive image classification without using most of the battery. Even the smallest edge devices can use AI effectively and work intelligently given the advancements in chip architecture and power control.

The end-user industry segment is divided into consumer electronics, automotive, healthcare, industrial, retail, smart cities, aerospace & defense and others. The consumer electronics segment dominated the market, with a share of around 37% in 2024. Smarter experiences are now possible on smartphones, smart speakers, wearable fitness trackers, tablets, smart TVs and home automation systems, mainly due to built-in AI features. Edge AI hardware has the highest potential for deployment because billions of consumer electronics are used around the world. Companies are turning to edge AI in consumer electronics mainly to ensure real-time data handling, faster solutions and more privacy. People are used to getting quick answers from voice assistants, on-the-fly translation into any language, improved photo editing and touchless or facial recognition and they can only get those benefits with the help of special AI hardware like NPUs and microchips inside each device. Since Edge AI processes data locally, there is less time to wait and more security for personal data. Advanced AI features being added by tech giants—Apple, Samsung, Google and Huawei—have encouraged people to use edge AI in everyday consumer gadgets. In order to work directly on devices, from AI apps to cameras and smart health monitors, chip companies spend much on new innovations. As edge AI technology becomes popular and users’ standards rise, consumer electronics will continue to drive its development, staying ahead in this field.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 5.77 Billion |

| Market size value in 2034 | USD 30.19 Billion |

| CAGR (2025 to 2034) | 18% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Component, Device Type, Power Consumption and End-User Industry |

As per The Brainy Insights, the size of the global edge AI hardware market was valued at USD 5.77 billion in 2024 to USD 30.19 billion by 2034.

Global edge AI hardware market is growing at a CAGR of 18% during the forecast period 2025-2034.

The market's growth will be influenced by technological advancements and other similar improvements.

High costs of production could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global edge AI hardware market based on below mentioned segments:

Global Edge AI Hardware Market by Component:

Global Edge AI Hardware Market by Device Type:

Global Edge AI Hardware Market by Power Consumption:

Global Edge AI Hardware Market by End-User Industry:

Global Edge AI Hardware Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date