- +1-315-215-1633

- sales@thebrainyinsights.com

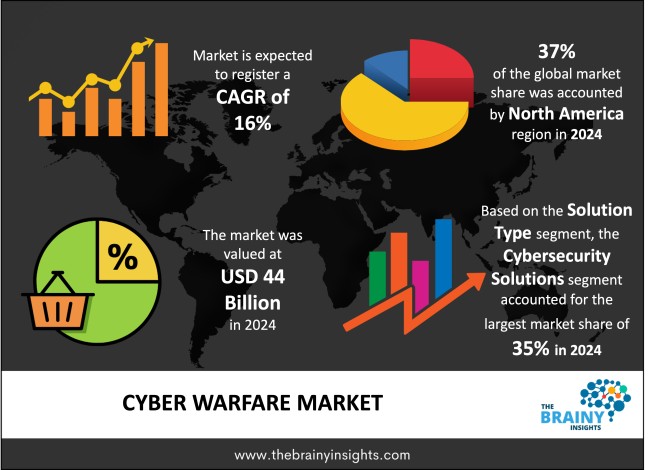

The global cyber warfare market was valued at USD 44 billion in 2024 and grew at a CAGR of 16% from 2025 to 2034. The market is expected to reach USD 194.10 billion by 2034. The rising number of cyberattacks and evolving nature of cyber threats will drive the growth of the global cyber warfare market.

Cyber warfare is a completely different type of warfare compared to conventional warfare. It is fought online, over computer systems, networks, critical digital infrastructure and the like. These attacks are either defensive or offensive and may be directed to render the communication, command and control capability, economic and military infrastructures of the enemy useless without any single shot fired. Fundamentally, cyber warfare entails a wide range of strategies including hacking, launch of malware, denial of service (DoS) operations, ransomware, spy and sabotage. Cyber warfare has become strategically important because the world has become dependent on the application of digital technologies. Nations consider cyber capabilities as part national defence and offence now, spending a fortune on cyber commands, intelligence collection, and building advanced cyber weapons. The cyber warfare enables asymmetrical projection of power which opens the scope of lesser states or non-state entities to cause havoc to a greater and technologically superior attacker, somehow even the playing field. In general, cyber warfare is a very multifaceted, rapidly developing field that comprises knowledge, strategy, as well as international law. It requires an active improvement in cybersecurity, foreign policy systems, and security systems so that the interests of the country can be secured and the world is stable in this digital era.

Get an overview of this study by requesting a free sample

The evolving nature of threats and security challenges – The most pressing issue for contemporary governments worldwide is the safety and security of national interests from cyberattacks and threats. It is significantly important to defend critical infrastructure, armed forces, and other sensitive sectors against the ever evolving advanced and sophisticated cyber-attacks. This makes the authorities invest a lot of money in the cyber warfare technology to protect their systems. The technological evolution is also a key factor given the continuous breakthroughs in the sphere of cybersecurity instruments, artificial intelligence, machine learning, and automated threat detection, the efficiency of cyber warfare is constantly increasing. As these technologies grow, governments authorities become more inclined to take up and implement them in their systems. Also, most nations are introducing modernization of defence forces that acknowledge cyber warfare as one of the key areas of action. These modernization processes can fuel the demand of state-of-the-art cyber offense and defence solutions. additionally, governments themselves are coming to acknowledge their digital weaknesses, particularly in the areas of government networks, and physical critical infrastructure and thus there is a necessity to fortify cyber defence mechanisms and retaliation capabilities. It leads to a high level of awareness, which promotes the constant investment in cyber warfare assets.

Financial and infrastructural limitations – The constraints that narrow the demand of cyber warfare are more largely centred to the financial, infrastructural and organizational capabilities of countries. High cost incurred through the development and maintenance of cyber warfare capabilities is one of the greatest limitations. Creation of resilient and robust cyber infrastructure requires heavy investments in sophisticated technologies, research and development, dedicated hardware and software and maintenance of the cyber infrastructure over a long period. To most nations and especially developing ones, these costs overwhelm the national budget and narrow the range of cyber warfare programs. The last severe impediment is the lack of qualified people. The cybersecurity skills shortage is a problem experienced globally and this means that governments cannot easily find and/or retain talented experts like ethical hackers, cyber analysts and digital forensics experts that are needed to operationalize cyber warfare plans. Also, there may exist institutional obstacles in the form of traditional organizations and bureaucracies, which will challenge the incorporation of cyber warfare into the national security systems.

The shifting geopolitical landscape – The rising instances of cyberattacks on nations given the ever volatile and tense geopolitical landscape drives the growing demand for cyber warfare. Through the increased digitalization of conflicts, nations are stepping up to cyber warfare as strategic instrument to assert authority without having to participate in a conventional war. Moreover, the recurrent and complex cyberattacks by competing states, terrorist organizations, and virtual crime groups, has driven the investments in cyber warfare by governments worldwide. This is also increased by the global move towards digital infrastructure. With the economy, military operations and the government services relying more on the connected digital systems, there is more damage that could be done by cyber-attacks, a likely situation forcing countries to implement some form of cyber warfare protection in order to guard government properties. Additionally, due to asymmetry of cyber war, smaller states and non-state actors are able to level with the larger states, which has led to extensive investments to ensure strategic parity. The attempt by international community to establish cyber norms, regulations and laws also exert pressure on the countries to build on their powerful cyber capabilities so that they could either abide or shape the global standards.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global cyber warfare market, with a 37% market revenue share in 2024.

The United States is especially active in this matter as it has not only large units dealing with cyber warfare (the U.S Cyber Command (USCYBERCOM) but also incorporates cyber capabilities into all of its armed services. The superiority of the region can also be supported by the huge investments made by the government in advancing state-of-the-art cyber-tools, AI-powered defence systems, and secure communications systems. In the face of growing geopolitical frictions and subsequent raging cases of cyber-attacks aimed at national interests, North America has designated the issue of cyber warfare as its top strategic interest. It also has quite a number of the most prominent cybersecurity and defence technology firms in the world that are actively cooperating with federal and military government entities to come up with advanced solutions in both the defensive and offensive cyber operations. The rate and magnitude of cyber war is greatly increased via these public-private collaborations as well. In addition, the North American region has developed an effective regulatory and policy environment regarding the importance of cyber resiliency, threat intelligence sharing, and the protection of critical infrastructure, and therefore, it is in a better position than before to combat the emerging threats to its digital landscape.

North America Region Cyber Warfare Market Share in 2024 - 37%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The solution type segment is divided into cybersecurity solutions, offensive cyber tools, defensive cyber tools, threat intelligence and surveillance and monitoring. The cybersecurity solutions segment dominated the market, with a market share of around 35% in 2024. Solutions of cybersecurity have been found to be the most dominant in the global cyber warfare market since they are the basis of the national defence policies. Due to advanced and recurring cyber threats, nations are putting much more emphasis on effective cybersecurity systems to safeguard confidential information in governments, military communication and systems, vital infrastructure, and command-and-control apparatuses. Solution to cybersecurity include a wide variety of resources such as firewalls, intrusion detection systems, endpoint security, encryption, threat intelligence, as well as vulnerability management, all of which are paramount to the prevention, detection and containment of cyberattacks. The ability of cybersecurity solutions to be applied not only in the military but in civil sectors such as energy, finance, and healthcare industries, which are becoming more and more valuable resources in national security systems makes it the dominant components in the market. Furthermore, cybersecurity measures are scalable and deployable than cyber offensive weapons, thus made available through more countries including those of low cyber capability. The constant development of the sphere of AI-based threat detection, cloud security, and real-time monitoring solutions also plays its role in growing this niche.

The deployment mode segment is divided on-premise, cloud-based and hybrid. The on-premise segment dominated the market, with a market share of around 37% in 2024. On-premise deployment model offers the highest degree of control, security, and flexibility. On-premise deployment enables defence organization to have wholly determined control of its digital assets, without the need to contract with some third-party cloud service provider. Such deployments will make sure that sensitive information is protected with well-defined accessibility. Among the significant merits of on-premise implementation is adapting security framework and structures on-demand to suit peculiarities of operations, especially, classified systems. Such customization is critical to the cyber warfare where the various missions might demand different configurations as well as access control. Moreover, the activity of numerous defence and intelligence organizations takes place in significantly regulated conditions, and on-premises solutions allow organizations to be confident in their adherence. Additionally, preference of the on-premise infrastructure is also encouraged by its resilience and reliability in the event of any disruption.

The application segment is divided defence and military, government agencies, critical infrastructure protection, financial services and communication networks. The defence and military segment dominated the market, with a market share of around 38% in 2024. Defence and military industry is the leading market in the world dealing with cyber warfare as it plays significant role of ensuring the national security, preserving geopolitical power, and countering the contemporary threats in the digital space. Cyber warfare empowers defence forces to collect intelligence, destabilize the enemy infrastructure, disempower communication system, and protect the cyberattacks intended to harm national interests. Consequently, cyber operations have become the fifth arena of violence, i.e., along with land, sea, air, and space, indicating their vitality role. Military and defence organizations have the funds, technical capabilities and operational mandates to take the front line in development and implementation of advanced cyber warfare equipment. Military is also in the commanding position since it has to defend against many varieties of attacks, not just espionage and sabotage, but full-blown cyberattacks by hostile powers or non-state actors. With the rising number and intensity of cyber wars or cyber conflicts amidst the international geopolitics, it is expected that the defence and military segment will remain the most active force in the cyber warfare market, in terms of demand, innovation and strategic leadership.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 44 Billion |

| Market size value in 2034 | USD 194.10 Billion |

| CAGR (2025 to 2034) | 16% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Type, Deployment Mode and Application |

As per The Brainy Insights, the size of the global cyber warfare market was valued at USD 44 billion in 2024 to USD 194.10 billion by 2034.

Global cyber warfare market is growing at a CAGR of 16% during the forecast period 2025-2034.

The market's growth will be influenced by the evolving nature of threats and security challenges.

Financial and infrastructural limitations could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global cyber warfare market based on below mentioned segments:

Global Cyber Warfare Market by Solution Type:

Global Cyber Warfare Market by Deployment Mode:

Global Cyber Warfare Market by Application:

Global Cyber Warfare Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date