- +1-315-215-1633

- sales@thebrainyinsights.com

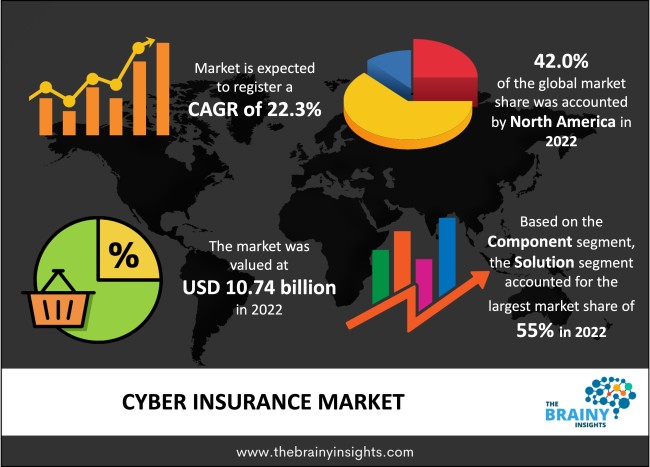

The global cyber insurance market was valued at USD 10.74 billion in 2022 and is anticipated to grow at a CAGR of 22.3% from 2023 to 2032. The dependence on technology and the internet has become crucial for organizations and individuals in today's more connected and digital society. While this technological development has many benefits and advantages, it has also ushered in a new era of hazards and liabilities, especially in cyber security. Business enterprises and the corporate sector are planning tactics to defend themselves against these potential cataclysms due to the prevalence of cyber-attacks, data breaches, and other cyber threats prevailing in the digital era. Cyber insurance, a new but fast-expanding technology within the overall insurance market, has become essential for controlling and minimizing the risks connected to the digital age.

The digital revolution has created a new innovation, connectivity, and connectivity era. The advent of cybercrime has also brought up new difficulties, disrupting the overall technology cycle and development. Cybercriminals use technology to carry out identity theft, ransom ware attacks, hacking and data breaches, and other types of criminal activity. These threats put people, corporate organizations, and governments at great risk as their property gets jeopardized. Cyber insurance is a specialized product developed by the insurance industry in response to the growing threat of cybercrime. Cybercrime has several aspects and refers to a wide range of illicit conduct made possible by using the internet and digital technology. The activities considered under cybercrimes include hacking, ransom ware attacks, data theft, spoofing, financial fraudulence, and spreading malicious software and other activities. Cybercriminals may have a variety of motives, ranging from monetary gain, biological warfare, and corporate espionage to political activism and others. Cybercrime has become universal and constantly transforming due to the widespread use of digital devices and the growing intersection of systems and data.

A certain insurance policy created to offer financial protection against losses brought on by cyber-related crimes is known as cyber insurance. Cyber insurance protects corporate organizations and individuals that risk reputational damage and financial loss because of cybercrimes and related activities. Online fraud, phishing, ransom ware attacks, and other activities are only a few examples of cybercrimes for which cyber insurance provides security. Cyber insurance is also known as cyber risk insurance. Cybercriminals are using smart strategies to exploit vulnerabilities because of ongoing technological advancements, which is why the landscape of cyber threats is constantly changing. The insurers must constantly modify their policies to account for new risks because cybercrimes are dynamic. One of the fundamental aspects that sets cyber insurance apart from traditional insurance is its capacity to change along with the rapidly evolving digital threat environment.

Get an overview of this study by requesting a free sample

Rising Incidences of Cybercrimes - The need for cyber insurance to safeguard against cybercrimes is a key driving force in the global cyber insurance market. The expanding cyber security landscape is one of the main factors propelling the growth of the global cyber insurance industry. Cybercriminals have advanced in sophistication and tenacity in exploiting weaknesses as technology advances. Data breaches, ransom ware attacks, and hacking are just a few of the cyber threats that have increased, raising awareness of the potential reputational and financial risks enterprises may encounter. The significance of cyber insurance has become increasingly popular due to high-profile cybercrimes happening across the globe. The serious effects of cybercrimes on a company's operations and brand reputation have worsened, and large-scale data breaches and cyber-attacks against well-known organizations have seriously impacted the overall brand image of any enterprise. As a result of these incidents, business enterprises are investing in cyber insurance to safeguard themselves against similar dangers and cyber threats in the current situation. This primary factor is boosting the market growth and development.

Lack of Standardization - For insurers, the accumulation of cyber risk presents a special difficulty. A single cyber catastrophe may simultaneously affect multiple policyholders, creating significant risk aggravation. A mass ransom ware assault that targets a particular industry, for instance, can result in a large number of claims from affected policyholders. To overcome this difficulty, insurers must carefully control their risk exposure and ensure they have enough insurance to cover potential catastrophic events. There is a lack of uniformity in cyber insurance policy forms, policies, and cost structures. Unlike traditional insurance markets, the cyber insurance market is distinguished by various policy offerings, where standardized policy formats and industry benchmarks are prevalent. Organizations may find it difficult to compare policies properly and understand the extent of the coverage they are acquiring due to a lack of standardization. It may also result in conflicts over the wording of the insurance and inconsistent claim handling. These factors are limiting the market growth and development.

Technological Advancements - The dynamic nature of cyber security threats and the need for insurers to be aware of new risks are driving the ongoing evolution of the global cyber insurance market. The industry is always changing in this ever-evolving environment, and technology advancements are essential. In the market for cyber insurance, data analytics and predictive modelling have become essential tools for insurers. With these technologies, insurers can directly analyze a tremendous quantity of data, including information on policyholders, cyber threat intelligence, and historical claims data, to spot patterns and trends in cyber risk. Insurers can modify coverage and pricing using predictive modelling to create more precise forecasts about the likelihood and severity of upcoming cyber threats. For instance, insurers can examine an organization's cyber security posture and vulnerabilities using predictive modelling, which enables them to make more accurate insurance decisions. Additionally, insurers may encourage policyholders to take effective security precautions using data analytics. This factor is expected to provide lucrative growth opportunities in the upcoming years.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America region emerged as the most prominent global cyber insurance market, with a 42.0% market revenue share in 2022. The region is considered the early adopter of cyber insurance due to the presence of the key players. In North America, 2021 witnessed more data theft incidents than the previous years. The country has had numerous data thefts throughout the years. More than 1,780 data breach indicators have been documented, according to a report published by the Identity Theft Resource Center in 2022. Business enterprises from various industries are encouraged to choose cyber security insurance due to the rising frequency of data breaches, which stimulates regional market growth. Additionally, due to the region's significant increase in connected devices, cyberattacks are increasing exponentially. This factor has resulted in cyber insurance adoption, promoting regional development in the present scenario. The regional market players also engage in various market strategies such as product innovation, product differentiation, mergers, acquisitions, partnerships, and strategic alliances to maintain their competitive edge.

North America Region Cyber insurance Market Share in 2022 - 42.0%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The component segment includes solutions and services. The solution segment accounted for the largest market share of around 55% in 2022. The solutions category includes insurance plans designed to deal with the financial consequences of cyber threats and crimes. These policies cover many situations, from first-party policies that shield policyholders from their direct losses to third-party policies that take care of liabilities resulting from cyber-attacks and other incidents to the loss of personal data. These insurance options can better gauge the company's cyber risk or hazard scope. The rise in cyber-attacks, invasions of privacy, and the impacts of the global epidemic were all factors that contributed to the sharp rise in data breaches. Therefore, various organizations and businesses use solutions to maintain corporate cyber security measures.

The insurance type segment is bifurcated into standalone and packaged. The standalone segment dominated, with a market share of around 59% in 2022. The standalone insurance assists business enterprises in reducing the risk of silent exposures. As standalone policies reduce the danger of silent exposures and strengthen the market, many cyber insurance companies are experiencing a change in policy consumers from endorsement to standalone insurance policies. These policies frequently provide liability coverage for losses resulting from data breaches. Business enterprises can also get financial compensation for their legal and investment costs and the damage caused when they file a standard policy claim related to a cyber incident. These plans also provide cover for any direct damages brought on by phishing, social engineering fraud, cyber fraud, spoofing, and phishing, as well as any legal obligations that organizations may have to third parties.

The organization size segment is divided into SMEs and large enterprises. The large enterprises segment dominated the market, with a market share of around 60% in 2022. Due to the ability to invest a higher budget for insurance and cyber security activities, large enterprises dominate the market. Large enterprises have the financial resources to invest in strong cyber security measures and all-encompassing insurance coverage to safeguard their operations, reputation, and customer confidence. The dominance of the large enterprise market results from this tendency to engage in cyber insurance. The necessity for cyber insurance and cyber security in large enterprises has increased due to the frequency of hacking assaults in major businesses. Cybercriminals have targeted large organizations; thus, these companies need to invest in providing insurance to protect themselves from these attacks. This is the primary factor for the segment growth.

The industry segment is classified into BFSI, healthcare, retail, transportation and others. The BFSI segment dominated the market, with a share of around 43% in 2022. Due to the vast customer base that the sector serves and the sensitive financial information at risk, the BFSI industry is one of the critical infrastructure categories that frequently exploit data breaches and cyber-attacks. Because the financial industry has a highly attractive operating model with extraordinary risks and the plus of relatively low risk and detectability, cybercriminals are optimizing a wide variety of evil cyber-attacks to paralyze it. The threat environment for these attacks includes Trojans, ATMs, ransom ware, data breaches, institutional invasion, data thefts, fiscal breaches, and other threats, increasing the need for cyber security insurance in the BFSI sector.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2022 | USD 10.74 Billion |

| Market size value in 2032 | USD 80.39 Billion |

| CAGR (2023 to 2032) | 22.3% |

| Historical data | 2019-2021 |

| Base Year | 2022 |

| Forecast | 2023-2032 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East & Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Component, Organization Size, insurance Type, Industry |

As per The Brainy Insights, the size of the cyber insurance market was valued at USD 10.74 billion in 2022 to USD 80.39 billion by 2032.

The global cyber insurance market is growing at a CAGR of 22.3% during the forecast period 2023-2032.

North America region became the largest market for cyber insurance.

The growing incidences of cybercrime followed by the importance of cyber insurance is influencing the market's growth.

1. Introduction

1.1. Objectives of the Study

1.2. Market Definition

1.3. Research Scope

1.4. Currency

1.5. Key Target Audience

2. Research Methodology and Assumptions

3. Executive Summary

4. Premium Insights

4.1. Porter’s Five Forces Analysis

4.2. Value Chain Analysis

4.3. Top Investment Pockets

4.3.1. Market Attractiveness Analysis by Component

4.3.2. Market Attractiveness Analysis by Industry

4.3.3. Market Attractiveness Analysis by Insurance Type

4.3.4. Market Attractiveness Analysis by Organization Size

4.3.5. Market Attractiveness Analysis by Region

4.4. Industry Trends

5. Market Dynamics

5.1. Market Evaluation

5.2. Drivers

5.2.1. Blockchain Distributed Ledger

5.3. Restraints

5.3.1. Lack of Standardization

5.4. Opportunities

5.4.1. Technological Advancements

6. Global Cyber insurance Market Analysis and Forecast, By Component

6.1. Segment Overview

6.2. Solution

6.3. Services

7. Global Cyber insurance Market Analysis and Forecast, By Industry

7.1. Segment Overview

7.2. BFSI

7.3. Healthcare

7.4. Retail

7.5. Transportation

7.6. Others

8. Global Cyber insurance Market Analysis and Forecast, By Insurance Type

8.1. Segment Overview

8.2. Standalone

8.3. Packaged

8.4. Hybrid

9. Global Cyber insurance Market Analysis and Forecast, By Organization size

9.1. Segment Overview

9.2. SMEs

9.3. Large Enterprises

10. Global Cyber insurance Market Analysis and Forecast, By Regional Analysis

10.1. Segment Overview

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.2.3. Mexico

10.3. Europe

10.3.1. Germany

10.3.2. France

10.3.3. U.K.

10.3.4. Italy

10.3.5. Spain

10.4. Asia-Pacific

10.4.1. Japan

10.4.2. China

10.4.3. India

10.5. South America

10.5.1. Brazil

10.6. Middle East and Africa

10.6.1. UAE

10.6.2. South Africa

11. Global Cyber insurance Market-Competitive Landscape

11.1. Overview

11.2. Market Share of Key Players in the Cyber Insurance Market

11.2.1. Global Company Market Share

11.2.2. North America Company Market Share

11.2.3. Europe Company Market Share

11.2.4. APAC Company Market Share

11.3. Competitive Situations and Trends

11.3.1. Product Launches and Developments

11.3.2. Partnerships, Collaborations, and Agreements

11.3.3. Mergers & Acquisitions

11.3.4. Expansions

12. Company Profiles

12.1. Chubb

12.1.1. Business Overview

12.1.2. Company Snapshot

12.1.3. Company Market Share Analysis

12.1.4. Company Product Portfolio

12.1.5. Recent Developments

12.1.6. SWOT Analysis

12.2. Travelers Indemnity Company

12.2.1. Business Overview

12.2.2. Company Snapshot

12.2.3. Company Market Share Analysis

12.2.4. Company Product Portfolio

12.2.5. Recent Developments

12.2.6. SWOT Analysis

12.3. American International Group, Inc.

12.3.1. Business Overview

12.3.2. Company Snapshot

12.3.3. Company Market Share Analysis

12.3.4. Company Product Portfolio

12.3.5. Recent Developments

12.3.6. SWOT Analysis

12.4. AXA XL

12.4.1. Business Overview

12.4.2. Company Snapshot

12.4.3. Company Market Share Analysis

12.4.4. Company Product Portfolio

12.4.5. Recent Developments

12.4.6. SWOT Analysis

12.5. Beazley Group

12.5.1. Business Overview

12.5.2. Company Snapshot

12.5.3. Company Market Share Analysis

12.5.4. Company Product Portfolio

12.5.5. Recent Developments

12.5.6. SWOT Analysis

12.6. CNA Financial Corporation

12.6.1. Business Overview

12.6.2. Company Snapshot

12.6.3. Company Market Share Analysis

12.6.4. Company Product Portfolio

12.6.5. Recent Developments

12.6.6. SWOT Analysis

12.7. AXIS Capital Holdings Limited

12.7.1. Business Overview

12.7.2. Company Snapshot

12.7.3. Company Market Share Analysis

12.7.4. Company Product Portfolio

12.7.5. Recent Developments

12.7.6. SWOT Analysis

12.8. BCS Financial Corporation

12.8.1. Business Overview

12.8.2. Company Snapshot

12.8.3. Company Market Share Analysis

12.8.4. Company Product Portfolio

12.8.5. Recent Developments

12.8.6. SWOT Analysis

12.9. Zurich Insurance

12.9.1. Business Overview

12.9.2. Company Snapshot

12.9.3. Company Market Share Analysis

12.9.4. Company Product Portfolio

12.9.5. Recent Developments

12.9.6. SWOT Analysis

12.10. The Hanover Insurance, Inc.

12.10.1. Business Overview

12.10.2. Company Snapshot

12.10.3. Company Market Share Analysis

12.10.4. Company Product Portfolio

12.10.5. Recent Developments

12.10.6. SWOT Analysis

12.11. Arthur J. Gallagher & Co.

12.11.1. Business Overview

12.11.2. Company Snapshot

12.11.3. Company Market Share Analysis

12.11.4. Company Product Portfolio

12.11.5. Recent Developments

12.11.6. SWOT Analysis

List of Table

1. Global Cyber insurance Market, By Component, 2019-2032 (USD Billion)

2. Global Solution, Cyber insurance Market, By Region, 2019-2032 (USD Billion)

3. Global Services, Cyber insurance Market, By Region, 2019-2032 (USD Billion)

4. Global Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

5. Global BFSI Cyber insurance Market, By Region, 2019-2032 (USD Billion)

6. Global Healthcare Cyber insurance Market, By Region, 2019-2032 (USD Billion)

7. Global Retail, Cyber insurance Market, By Region, 2019-2032 (USD Billion)

8. Global Transportation, Cyber insurance Market, By Region, 2019-2032 (USD Billion)

9. Global Others Cyber insurance Market, By Region, 2019-2032 (USD Billion)

10. Global Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

11. Global Standalone Cyber insurance Market, By Region, 2019-2032 (USD Billion)

12. Global Packaged Cyber insurance Market, By Region, 2019-2032 (USD Billion)

13. Global Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

14. Global SMEs Cyber insurance Market, By Region, 2019-2032 (USD Billion)

15. Global Large Enterprises Cyber insurance Market, By Region, 2019-2032 (USD Billion)

16. Global Cyber insurance Market, By Region, 2019-2032 (USD Billion)

17. North America Cyber insurance Market, By Component, 2019-2032 (USD Billion)

18. North America Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

19. North America Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

20. North America Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

21. U.S. Cyber insurance Market, By Component, 2019-2032 (USD Billion)

22. U.S. Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

23. U.S. Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

24. U.S. Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

25. Canada Cyber insurance Market, By Component, 2019-2032 (USD Billion)

26. Canada Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

27. Canada Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

28. Canada Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

29. Mexico Cyber insurance Market, By Component, 2019-2032 (USD Billion)

30. Mexico Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

31. Mexico Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

32. Mexico Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

33. Europe Cyber insurance Market, By Component, 2019-2032 (USD Billion)

34. Europe Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

35. Europe Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

36. Europe Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

37. Germany Cyber insurance Market, By Component, 2019-2032 (USD Billion)

38. Germany Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

39. Germany Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

40. Germany Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

41. France Cyber insurance Market, By Component, 2019-2032 (USD Billion)

42. France Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

43. France Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

44. France Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

45. U.K. Cyber insurance Market, By Component, 2019-2032 (USD Billion)

46. U.K. Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

47. U.K. Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

48. U.K. Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

49. Italy Cyber insurance Market, By Component, 2019-2032 (USD Billion)

50. Italy Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

51. Italy Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

52. Italy Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

53. Spain Cyber insurance Market, By Component, 2019-2032 (USD Billion)

54. Spain Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

55. Spain Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

56. Spain Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

57. Asia Pacific Cyber insurance Market, By Component, 2019-2032 (USD Billion)

58. Asia Pacific Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

59. Asia Pacific Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

60. Asia Pacific Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

61. Japan Cyber insurance Market, By Component, 2019-2032 (USD Billion)

62. Japan Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

63. Japan Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

64. Japan Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

65. China Cyber insurance Market, By Component, 2019-2032 (USD Billion)

66. China Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

67. China Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

68. China Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

69. India Cyber insurance Market, By Component, 2019-2032 (USD Billion)

70. India Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

71. India Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

72. India Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

73. South America Cyber insurance Market, By Component, 2019-2032 (USD Billion)

74. South America Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

75. South America Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

76. South America Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

77. Brazil Cyber insurance Market, By Component, 2019-2032 (USD Billion)

78. Brazil Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

79. Brazil Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

80. Brazil Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

81. Middle East and Africa Cyber insurance Market, By Component, 2019-2032 (USD Billion)

82. Middle East and Africa Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

83. Middle East and Africa Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

84. Middle East and Africa Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

85. UAE Cyber insurance Market, By Component, 2019-2032 (USD Billion)

86. UAE Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

87. UAE Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

88. UAE Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

89. South Africa Cyber insurance Market, By Component, 2019-2032 (USD Billion)

90. South Africa Cyber insurance Market, By Industry, 2019-2032 (USD Billion)

91. South Africa Cyber insurance Market, By Insurance Type, 2019-2032 (USD Billion)

92. South Africa Cyber insurance Market, By Organization size, 2019-2032 (USD Billion)

List of Figures

1. Global Cyber insurance Market Segmentation

2. Cyber insurance Market: Research Methodology

3. Market Size Estimation Methodology: Bottom-Up Approach

4. Market Size Estimation Methodology: Top-Down Approach

5. Data Triangulation

6. Porter’s Five Forces Analysis

7. Value Chain Analysis

8. Global Cyber insurance Market Attractiveness Analysis by Component

9. Global Cyber insurance Market Attractiveness Analysis by Industry

10. Global Cyber insurance Market Attractiveness Analysis by Insurance Type

11. Global Cyber insurance Market Attractiveness Analysis by Organization size

12. Global Cyber insurance Market Attractiveness Analysis by Region

13. Global Cyber insurance Market: Dynamics

14. Global Cyber insurance Market Share by Component (2023 & 2032)

15. Global Cyber insurance Market Share by Industry (2023 & 2032)

16. Global Cyber insurance Market Share by Insurance Type (2023 & 2032)

17. Global Cyber insurance Market Share by Organization size (2023 & 2032)

18. Global Cyber insurance Market Share by Regions (2023 & 2032)

19. Global Cyber insurance Market Share by Company (2022)

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. The Brainy Insights has segmented the global cyber insurance market based on below-mentioned segments:

Global Cyber Insurance Market by Component:

Global Cyber Insurance Market by Insurance Type:

Global Cyber Insurance Market by Industry:

Global Cyber Insurance Market by Organization Size:

Global Cyber Insurance Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date