- +1-315-215-1633

- sales@thebrainyinsights.com

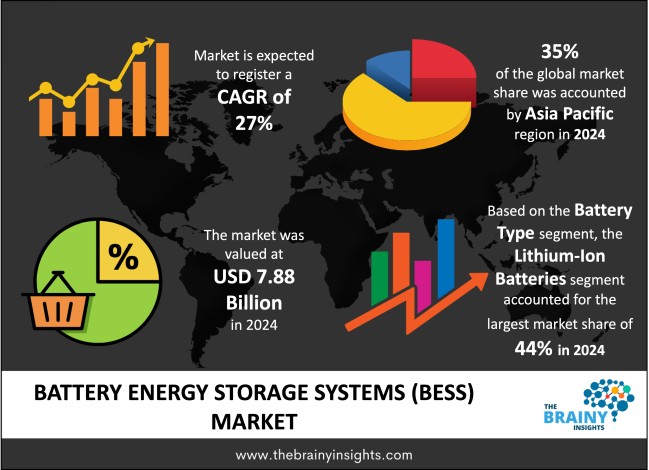

The global battery energy storage systems (BESS) market was valued at USD 7.88 billion in 2024 and grew at a CAGR of 27% from 2025 to 2034. The market is expected to reach USD 86.01 billion by 2034. The increasing energy demands will drive the growth of the global battery energy storage systems (BESS) market.

The Battery Energy Storage Systems (BESS) market forms a quickly expanding part of the global energy market, which is fuelled by the increasing demand to rely on trustworthy, adaptable, and clean energy choices. BESS are the storage systems that use rechargeable batteries to store power and use it later when it is needed, and it plays a vital role of balancing the supply and demand, improving grid stability and helping to increase renewable energy generation such as solar and wind. The systems are becoming essential in contemporary energy infrastructure, because they can be used to offer backup, frequency regulation, load shifting and peak shaving of power. Li-ion Batteries are presently the most common in BESS market due to high power density, longer lifecycle, and the falling prices. The landscape is however slightly diversifying gradually with the development of alternative batteries like the flow battery, sodium-ion, and solid-state batteries. Several factors such as the rising projects of renewable energy systems, growing energy demand, pro-government policies and technology improvements are driving the market. With the world moving to use of low-carbon energy systems, the market of battery energy storage will be of much significance in determining future of energy- flexibility, reliability, and sustainability.

Get an overview of this study by requesting a free sample

Technological advancements and operational enhancements – The internal forces that spurred the need to have Battery Energy Storage Systems (BESS) are mostly anchored in the technological, operational, and the market forces in the energy industry. The growth in the placing of renewable energy sources like solar and wind into the electrical grid can be considered one of the most important drivers. These sources are intermittent in nature hence BESS are a crucial role in ensuring that there is sufficient electricity supply and the supply is steady and reliable by storing excess energy and releasing the same when required. The increase in market growth is also being driven by technological improvements in the design, efficiency, and safety of battery industry, especially in the lithium-ion battery and the other upcoming chemistries such as solid-state and flow batteries. The innovations have not only increased the energy density and battery lifecycle it has also increased performance when subjected to different loads. The other significant internal development is the drastic forced decrease in the cost of batteries in the last ten years, making energy storage solutions economically beneficial in the residential, commercial, and utility scale segments. Besides, the use of BESS is becoming a part of grid modernization options. They are indispensable parts of smart grids with their capacity to offer services like peak shaving and load shifting along with frequency regulation and voltage support. Companies and industries are using BESS to secure energy and cut down on reliance on the conventional grid power and thereby prevent operational halts like outages.

High cost of BESS – The high cost of purchasing and installing the battery storage systems especially in the utility-scale is one of the major challenges. Though the cost of batteries has now reduced by time, the whole system cost; this entails inverters, control systems and installations are high such that it is less available to small scale or frugal economic users. The other major shortcoming is that batteries have short lifespan and they diminish in performance. The energy efficiency and storage capacity will decline with charge-discharge cycles over time making cost of maintenance higher as well as requiring replacement. Another impeding factor is related to safety issues, especially when dealing with lithium-ion batteries, as they are prone towards overheating, thermal runaway, and fire when unmanaged. Such security concerns may be a deterrent to adoption in residential locations and other essential facilities. Furthermore, special skills, software and system customization required drive up costs of operations and restrict usage to non-technical users.

Environmental and regulatory factors – The macroeconomic, environmental, and regulatory trends affecting the global energy market are driving the demand of Battery Energy Storage Systems (BESS). Among the most notable developers is the growing government regulatory pressure to shift towards clean energy. A lot of nations are already adopting favourable policies, incentives, and regulation mechanism, including renewable energy targets and tax credits, renewable energy, and energy storage mandates which will augment the market’s growth. Moreover, the global energy demand is experiencing rapid growth, particularly, in fast urbanizing and industrializing areas, thus exerting more pressure on the available power infrastructure forcing the need to have flexible and decentralized energy storage systems. The second important force is climate change that is imposing governments, industries, and consumers to be more sustainable and resilient. BESS assist in minimizing the usage of fossil fuels. Uncertainties related to geopolitical developments and the uncertain fossil fuel prices are also creating an incentive for the countries to boost energy security and self-sufficiency, which further justify investments in local energy storage systems. Moreover, the urbanization rate and electrification rate of the world into EV, smart home, and all things digital are creating higher and more consistent requirements of high-quality power with reliable supply which can be easily accomplished with BESS.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. Asia Pacific emerged as the most significant global battery energy storage systems (BESS) market, with a 35% market revenue share in 2024.

Asia-Pacific (APAC) represents the most powerful region in the international Energy Storage Systems (BESS) market and this can be clarified by the mix of excellent governmental encouragement, greatly expanding renewable energy capacity, and growing industrial and residential electricity requirements. China, Japan, South Korea, Australia, and many other countries are adopting BESS technology to help them modernize the power system and achieve such their respective decarbonization plans. China, more specifically, enjoys a considerable market share because of their tremendous investments in renewable energy projects and their aggressive propositions on reducing carbon emissions and increasing energy security. The manufacturing ecosystem of the country which is well prepared to produce lithium-ion batteries further boosts its control as it reduces the expense and facilitates large-scale implementations. Besides China, other APAC countries also are increasing energy storage capacities to overcome the problems of grid reliability because of the growth of renewable integration and urbanization. Regional governments are also introducing favourable policies, subsidy and regulatory structures that favour both utility-scale and behind-the-meter storage solutions.

Asia Pacific Region Battery Energy Storage Systems (BESS) Market Share in 2024 - 35%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The battery type segment is divided into lithium-ion batteries, lead-acid batteries, flow batteries, sodium-sulphur batteries and others. The lithium-ion batteries segment dominated the market, with a market share of around 44% in 2024. Lithium-ion batteries have taken leadership in the global Battery Energy Storage Systems (BESS) market with the highest share of the market in terms of the scale of energy in the utility scale and behind-the-meter markets. It is mainly predisposed to this dominance by their favourable performance features such as high energy density, lightweight, long cycle life, and high charge rates. The characteristics of lithium-ion batteries render them exceedingly suitable to an expansive variety of applications, such as grid parametrization and renewable energy integration, or residential backup power and electric vehicle (EV) subsistence systems. Of all battery chemistries, lithium-ion is the most cost-effective one in terms of efficiency and scalability, and that has made the battery chemistry popular. The second reason as to why they are dominating is the swift reduction in lithium-ion technology, as it is mainly due to the economies of scale through mass production brought by the manufacturers of EVs. The further improvements made on the safety, reliability and lifecycle of the lithium-ion batteries can be attributed to technological developments and the innovation on work front in battery management systems (BMS), thermal control and energy efficiency. Besides, lithium-ion batteries require less effort when it comes to procurement and implementation due to the global supply chain that was built, high availability, and robust R&D base in support of the battery chemistry. More so, lithium-ion batteries also have a compact form factor with modularity that will enable flexible system design and installation even within space-limited facility spaces.

The connection type segment is divided into on-grid and off-grid. The on-grid segment dominated the market, with a market share of around 62% in 2024. The on-grid unit controls the overall market of Battery Energy Storage Systems (BESS) in the world because it is of paramount importance in terms of assisting the modern power grid to work and meeting the needs of having integrations of renewable energy resources. On-grid, or grid-connected BESS, refers to systems that are directly connected to the main electricity grid, where either excess energy can be pushed onto the grid according to demand or the desired energy can be pulled-off the grid in order to charge the power system. The advantage of this architecture is that the benefit is notable in utility-scale applications, where the storage is applied in stabilizing the voltage, peak loading, and maintenance of constant and balanced power delivery in response to variability in renewable energy generation caused by solar and wind energy supply. The world-changing dynamic toward the modernization and decarbonization of grid is one of the basic forces that made this segment dominant. Additionally, the on-grid BESS projects are more likely to receive regulatory support and government financing, especially in territories, such as Asia-Pacific, North America, and Europe, where there are already significant plans on the adopted energy transformation. Such scalability, that is achieved in on-grid storage systems, as well as their centralized control and economic benefits contribute to a broad implementation of those systems further. Consequently, on-grid BESS will continue to serve large-scale energy storage requirements, and thus they will continue to dominate the market in the world.

The energy capacity segment is divided into above 500 MW, 100–500 MW and below 100 MW. The above 500 MW segment dominated the market, with a share of around 39% in 2024. Such large capacity systems are mostly used in utility-scale projects, where the capacity to store and launch large quantities of electricity are essential in managing the supply and demand span across vast geographical locations. As renewable sources such as solar and wind generation become more pervasive, but by their nature intermittent, grid operators can rely on large-capacity BESS to store the excess generation and draw upon it during times of peak demand and is, therefore, a source of a stable and consistent power source. The scale of operation also enhances the competitiveness of this segment since big installations generally offer better cost per megawatt-hour, better system efficiency and standardization, and better cost to maintain and operate. Moreover, the rapid development of batteries chemistries and system integration has shown it possible and cost effective to implement such massive storage hardware. The above 500 MWh segment is therefore the fastest growing segment and it is well placed as a keystone of the international energy transition and the grid architecture of the future.

The end-user segment is divided into utilities, commercial, residential and industrial. The utilities segment dominated the market, with a share of around 57% in 2024. Utilities play a key role in the running and management of electric distribution and transmission systems, which makes them the most natural owners and operators of large-scale energy storage systems. Utilities aim at using BESS to resolve some key challenges posed by the rising number of intermittent renewable energy sources such as wind and solar. Through the use of battery storage, utilities will be able to do away with the volatility of the supply, balance loads, and improve grid reliability to ensure a steady and smooth supply of power to the consumers. The capability to offer grid services, in the form of frequency regulation, voltage support, and peak load shaving defines BESS as essential to smooth up-to-date grid management. The other contribution to the supremacy of utilities is their ability to invest in high capital and big projects which at the initial stages of implementation need high levels of capital outlay thus creating long-term advantages in terms of operations. The utilities can access the finances, regulatory interests, and engineering skills to build and operate high-complexity BESS infrastructure unlike individual consumers or small commercial organizations. The utilities also enjoy the cost advantages of economy of scale, centralized control, and integration of energy capabilities to optimise towards large geographical regions and end-users. Besides, favourable government regulations and policies tend to favour utilities when it comes to energy storage deployment proposals in the form of subsidies, mandates, and other efforts related to market reconciliations aimed at speeding the shift to clean energy.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 7.88 Billion |

| Market size value in 2034 | USD 86.01 Billion |

| CAGR (2025 to 2034) | 27% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Battery Type, Connection Type, Energy Capacity and End-User |

As per The Brainy Insights, the size of the global battery energy storage systems (BESS) market was valued at USD 7.88 billion in 2024 to USD 86.01 billion by 2034.

Global battery energy storage systems (BESS) market is growing at a CAGR of 27% during the forecast period 2025-2034.

The market's growth will be influenced by technological advancements and operational enhancements.

High cost of BESS could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global battery energy storage systems (BESS) market based on below mentioned segments:

Global Battery Energy Storage Systems (BESS) Market by Battery Type:

Global Battery Energy Storage Systems (BESS) Market by Connection Type:

Global Battery Energy Storage Systems (BESS) Market by Energy Capacity:

Global Battery Energy Storage Systems (BESS) Market by End-User:

Global Battery Energy Storage Systems (BESS) Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date