- +1-315-215-1633

- sales@thebrainyinsights.com

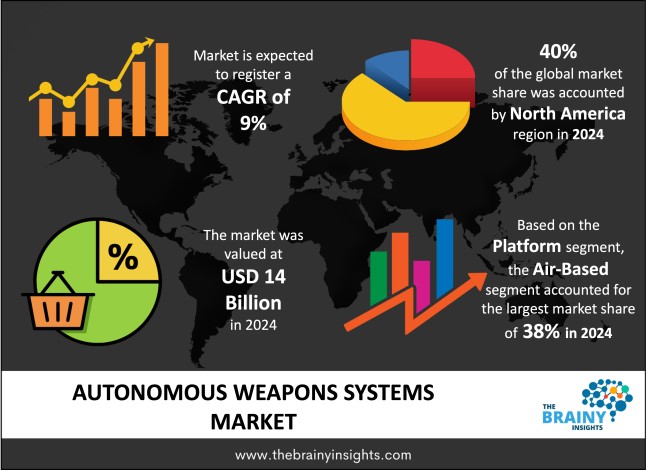

The global autonomous weapons systems market was valued at USD 14 billion in 2024 and grew at a CAGR of 9% from 2025 to 2034. The market is expected to reach USD 33.14 billion by 2034. The rapid automation and digitization globally will drive the growth of the global autonomous weapons systems market.

Autonomous weapons systems (AWS) are powerful weapons systems in the military sector that can both recognize, pursue, and attack targets without human interference. Such systems are based on artificial intelligence, machine learning applications, sensors, and data processing, which allows them to operate autonomously on ground, sea, air, or cyberspace. AWS may be deployed anywhere between defensive (e.g. missile interception systems) and offensive (e.g. autonomous drones, robotic tank, and loitering munitions (e.g. kamikaze drones)). Their outstanding feature is the speed of operations, accuracy, range, resilience and the ability to operate in high-risk areas where human troops cannot safely work. Autonomous weapons with a proper design would limit errors by humans, fewer casualties due to their higher accuracy, and make response time faster. The future of autonomous weapons systems will increasingly be dependent on the technologically enhanced breakthroughs, the international framework of governance, and an ethical agreement or consensus in the military and legal domain.

Get an overview of this study by requesting a free sample

Technological advancements and modernization of defence- The fast development of artificial intelligence, new machine learning and sensor technologies can be considered one of the most important driving forces as it allows AWS to work with more accurate data, higher speed, and more autonomously. Such inventions increase the competence of unmanned systems as they are able to detect, monitor and eliminate threats with limited human intervention. Besides, AWS are viewed as cost-efficient means in the long run due to decreasing the necessity of human presence in hazardous surroundings, a minimization of casualties and an opportunity of working on a 24/7 basis without tiring. Another factor that would play into the hands of AI adoption is that many countries are expanding their military budgets, and in particular, they want to modernize their military services by introducing the use of autonomous and AI-powered platforms. This increased salvo in internal funding is allowing the testing, development and implementation of next-generation systems. Moreover, AWS are force multipliers and allow smaller units to accomplish more with more visibility, faster reaction time and increased area of operation.

Operational, technological and financial limitations – The current technologies used in AWS are far from being complete, one can note the shortcomings related to target recognition, an ability to act in real-time, and the process of decision-making in dynamic battlefields. Such systems are not very effective in telling who is the combatant and who is a civilian, particularly on a complex or urban terrain hence possibility of serious issues of the reliability and safety of such systems arises. Smart sensors, processors, AI algorithms, and cybersecurity systems are prohibitively expensive, especially in those countries that have a small defence budget. Another big challenge is integration of autonomous systems with the already existing military infrastructure. Moreover, the system of AWS is also exposed to cyber threats, such as hacking, spoofing of GPS, and corruption of information, increasing the likelihood of failure or control of adversaries. These weaknesses raise more doubts regarding the reliability and safety of the use of such systems in the actual combat.

Changes in the global security landscape – The development of more regional and international conflicts is one of the most notable accelerators that have forced different countries to demand high-tech military solutions. AWS are especially useful in the asymmetric warfare scenario, where the state would have to face irregular forces, insurgents or even terrorist organizations. The current worldwide weapons competition, especially between the key players, including the United States of America, China, and Russia, contributes to the further intensification of the AWS development and implementation, as the countries intend to preserve the technological edge and strategic deterrence. Moreover, the international defence sector is also experiencing an increased demand in AWS exports, as states in the Middle East, Asia-Pacific, and Eastern Europe propose to improve their military potential with the help of sophisticated, AI-powered capabilities.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most significant global autonomous weapons systems market, with a 40% market revenue share in 2024.

The U.S. Department of Defence has long been interested in advancing and incorporating AI and autonomous systems in its military operation. Lockheed Martin, Northrop Grumman, Raytheon Technologies, and General Dynamics are some of the most diverse and innovative defence industries in the world that operate in the region and are on the front line designing and manufacturing state-of-the-art autonomous systems. In addition, the North American region enjoys a positive regulation and innovation environment that facilitates the speed of testing, prototyping, and implementation of autonomous technologies. The effort increases AWS adoption primarily because the U.S. Army has considerable presence worldwide and continues to undertake various combat and deterrence operations across a broad range of conflict areas.

North America Region Autonomous Weapons Systems Market Share in 2024 - 40%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The platform segment is divided into air-based, land-based, sea-based and space-based. The air-based segment dominated the market, with a market share of around 38% in 2024. The air-based autonomous weapons systems (AWS) have been taking the lion share in the global market given their versatility, speed, range, and strategic advantage in the contemporary wars. They are very essential to the military operations due to their capability to be used in an offensive and defensive manner. Among all the advantages of the use of air-based AWS, one can distinguish its provision of access and functioning in hostile or inaccessible settings without putting the human life at risk. They are easily movable, can be utilized even above extended periods of time and also in broad geographical distances, which makes the most appropriate in real time intelligence collection and in tactical operations. Moreover, the air-based systems have the advantage of swift technological development in the field of AI, sensors, propulsion and communication technologies, which increase their self-sufficiency, precision, and integrity. Their scalability and flexibility, as well, have made them popular.

The type segment is divided into semi-autonomous and fully autonomous. The semi-autonomous segment dominated the market, with a market share of around 57% in 2024. These systems run with considerable levels of autonomy as far as navigation, target detection, tracking is concerned, and still at the level of making decisions pertinent to the application of lethal force or target engagement. Such a “human-in-the-loop” solution eliminates a vast number of ethical, legal, and operationally related issues that are present with entirely autonomous systems. The incidence of semi-autonomous technologies within military organizations across the world is greater nowadays due to the fact that such technologies are compliant with the existing rules of engagement and the international humanitarian law that focus on human responsibility in decision-making during a military conflict. Besides, semi-autonomous systems are even more reliable and predictable since they balance machine efficacy and human discretion, posing a lower danger of inadvertent escalation or even harm the civilians. These systems have already been widely introduced in many of the platforms, such as drones, missile defence systems, and ground-based robotic deployed systems, and are deemed profitable in the conventional warfare aspect as well as the asymmetric war aspect. Also, based on a development perspective, semi-autonomous vehicles are simpler and less expensive than fully autonomous vehicles, thereby making them appealing even to middle-income countries.

The product segment is divided into missiles, guided rockets, combat UAVs, autonomous submarines, radar and sensors and software. The missiles segment dominated the market, with a market share of around 35% in 2024. The weapon category that prevails in the world market of autonomous weapons systems (AWS) is the missile category because the precision levels of the missiles are high, missiles are strategically significant, and they are also deployed extensively in the global defence sector. Artificial intelligence, real-time target recognition and adaptive guidance technologies are developing in applications to autonomous and semi-autonomous missile systems, including cruise missiles, loitering munitions and smart munitions. The supremacy of missiles is also facilitated by the fact that they are versatile since they can effectively work on different platforms namely air, on land, and in the seas plus that they can be used both in the offense and in the defence. The world of military is putting a lot of money and resources in the next generation missile that have autonomy to get a better range, speed, evasions, and accuracy qualities. Besides, autonomous missile systems form the important part of the integrated air defence network and deterrence policies, thus, becoming the part of the national security doctrines. The fact that they are relatively small in size and can be launched through various platforms, and have demonstrated their effectiveness in recent wars and conflicts has raised their demand the world over.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2024 | USD 14 Billion |

| Market size value in 2034 | USD 33.14 Billion |

| CAGR (2025 to 2034) | 9% |

| Historical data | 2021-2023 |

| Base Year | 2024 |

| Forecast | 2025-2034 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East and Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Platform, Type and Product |

As per The Brainy Insights, the size of the global autonomous weapons systems market was valued at USD 14 billion in 2024 to USD 33.14 billion by 2034.

Global autonomous weapons systems market is growing at a CAGR of 9% during the forecast period 2025-2034.

The market's growth will be influenced by technological advancements and modernization of defence.

Operational, technological and financial limitations could hamper the market growth.

This study forecasts revenue at global, regional, and country levels from 2021 to 2034. The Brainy Insights has segmented the global autonomous weapons systems market based on below mentioned segments:

Global Autonomous Weapons Systems Market by Platform:

Global Autonomous Weapons Systems Market by Type:

Global Autonomous Weapons Systems Market by Product:

Global Autonomous Weapons Systems Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date