- +1-315-215-1633

- sales@thebrainyinsights.com

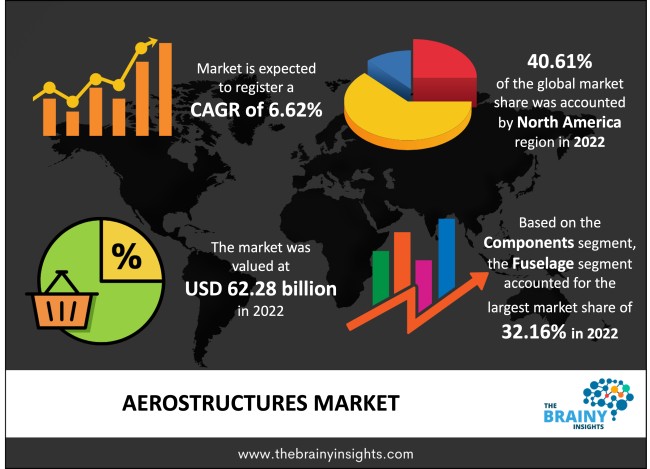

The global Aerostructures market generated USD 62.28 billion revenue in 2022 and is projected to grow at a CAGR of 6.62% from 2023 to 2032. The market is expected to reach USD 118.23 billion by 2032. The global expansion of commercial aircraft deployment is a significant catalyst driving the market's growth. The market growth is further fueled by an upswing in domestic and international tourism and stringent government regulations ensuring air safety. Additionally, the economic upturn in developing nations and substantial investments in developing performance-oriented and lightweight aerostructures play an equally pivotal role in fostering market growth.

Aerostructures constitute the fundamental components and elements that form the physical framework of an aircraft, defining its aerodynamic shape and ensuring structural stability during flight. Key elements within aerostructures include wings, fuselage, empennage (tail section), and supporting structures, all meticulously designed to optimize aerodynamic performance and structural integrity. Collectively, these components contribute to an aircraft's ability to achieve and maintain flight, influencing critical factors such as stability, manoeuvrability, and overall efficiency. The design and engineering of aerostructures involve carefully balancing materials, weight distribution, and adherence to rigorous safety standards and aviation regulations. Within the dynamic field of aviation, aerostructures play a central role in shaping aircraft characteristics, influencing fuel efficiency, and impacting the overall operational effectiveness of flight. Advancements in aerostructure design often involve incorporating innovative materials, state-of-the-art manufacturing processes, and the integration of cutting-edge technologies, all aimed at achieving optimal performance, safety, and sustainability in modern aircraft. The continuous evolution of aerostructures reflects the ongoing commitment of the aerospace industry to push the boundaries of design and engineering for enhanced aviation capabilities.

Get an overview of this study by requesting a free sample

Rising Demand for Commercial Aircraft - The increasing global demand for air travel has led to a surge in orders for new commercial aircraft. This demand drives the need for advanced aerostructures to enhance fuel efficiency, reduce weight, and improve overall performance.

Advancements in Material Technologies - Ongoing advancements in materials, such as composite materials and lightweight alloys, play a crucial role in the aerostructures market. These materials offer improved strength-to-weight ratios, contributing to fuel efficiency and lessening the environmental effect of aviation.

Stringent Fuel Efficiency and Emission Regulations - Stringent regulations imposed by aviation authorities worldwide to enhance fuel efficiency and reduce emissions are compelling aerospace manufacturers to invest in innovative aerostructures. Lightweight materials and aerodynamic designs are essential for meeting these regulatory requirements.

High Development and Manufacturing Costs - The development and manufacturing of advanced aerostructures involve substantial costs, including research and development expenses, raw material costs, and the expenses associated with adopting cutting-edge technologies. High initial investments can be a significant restraint, particularly for smaller aerospace companies.

Cyclical Nature of the Aerospace Industry - The aerostructures market is highly cyclical, influenced by economic conditions, geopolitical factors, and fluctuations in defence budgets. During economic slowdown or reduced defence spending, demand for new aircraft and aerostructures may decline, impacting the market growth.

Rising Global Air Travel Demand - The increasing need for air travel, driven by population growth, rising middle-class incomes, and expanding tourism, creates opportunities for aerostructure manufacturers to supply components for new aircraft.

Ongoing Developments Urban Air Mobility (UAM) - The ongoing advancements of urban air mobility solutions, including eVOLT aircraft, open new markets for aerostructure manufacturers. Lightweight and efficient structures are essential for the success of these innovative air transportation concepts.

Increased Defense Spending - Growing defense budgets in various countries create opportunities for aerostructure manufacturers to supply components for military aircraft. Defense modernization programs and the development of next-generation fighter jets contribute to the demand for advanced aerostructures.

Supply Chain Disruptions - The aerostructures market depends on a complicated global supply chain, making it vulnerable to disturbances driven by natural disasters, geopolitical tensions, or transportation issues. These disturbances can lead to delays and increased costs.

Trade Tariffs and International Trade Tensions - Trade tariffs and geopolitical tensions can affect the international aerospace supply chain. Changes in trade policies or restrictions can disrupt the flow of materials and components, creating uncertainties and challenges for aerostructure manufacturers.

The regions analyzed for the market include North America, Europe, South America, Asia Pacific, the Middle East, and Africa. North America emerged as the most prominent global Aerostructures market, with a 40.61% market revenue share in 2022.

North America, particularly the United States, has a long-established and robust aerospace industry. The presence of big aerospace players, such as Boeing and Lockheed Martin, contributes to the region's dominance in aerostructure manufacturing. Furthermore, the region is home to some of the world's leading aircraft manufacturers, including Boeing and Airbus (which has a significant presence in North America). These companies drive the demand for advanced aerostructures, and their manufacturing facilities are concentrated in the region. The region also hosts numerous research and innovation centers focused on aerospace technologies. Research and development (R&D) investments foster innovation in aerostructures, giving North American companies a competitive edge in producing cutting-edge solutions. Additionally, the United States has the world's largest defense budget, leading to a strong emphasis on developing and producing military aircraft. The demand for advanced aerostructures in the defense sector further strengthens North America's position in the global market. Moreover, North American aerospace companies often engage in strategic alliances and partnerships with domestic and international entities. These collaborations enhance the region's aerostructure development, production, and export capabilities. Besides, North American aerospace companies have established a global network of suppliers, providing a reliable and efficient supply chain. This network facilitates the timely and cost-effective production of aerostructures, contributing to market dominance.

North America Region Aerostructures Market Share in 2022 - 40.61%

www.thebrainyinsights.com

Check the geographical analysis of this market by requesting a free sample

The components segment is classified into empennage, fuselage, flight control surfaces, nacelle & pylon, nose, wings and others. The fuselage segment dominated the market, with a share of around 32.16% in 2022. The fuselage is an aircraft's central and critical component, providing the structural framework for accommodating passengers, crew, and cargo. As such, it constitutes a substantial portion of the overall aerostructure, contributing significantly to the market. In addition, the continuous growth in air travel demand and the need for new aircraft contribute to the dominant role of fuselage manufacturing in the aerostructures market. As airlines and manufacturers strive to meet the rising demand, the production of fuselages becomes a focal point. Furthermore, the fuselage integrates various advanced technologies, including avionics, connectivity systems, and structural enhancements. Manufacturers focus on incorporating these technologies into the fuselage design, adding value to the overall aircraft and driving demand for advanced aerostructures.

The aircraft type segment is divided into fixed-wing aircraft and rotary-wing aircraft. The fixed-wing aircraft segment is further divided into business jet, commercial, general aviation aircraft and military. The rotary-wing aircraft segment is sub-categorized into commercial helicopters, military helicopters, and UAVs. The fixed-wing aircraft segment dominated the market, with a share of around 72.35% in 2022. Fixed-wing aircraft are the primary modes of transportation for both passengers and cargo. The capability to transport big numbers of passengers and substantial cargo payloads makes fixed-wing aircraft essential for long-haul and intercontinental travel, contributing to their dominance in aerostructure demand. Additionally, fixed-wing aircraft are widely used in military applications, including fighter jets, bombers, reconnaissance planes, and transport aircraft. The military aviation sector drives substantial demand for advanced aerostructures, supporting the dominant role of fixed-wing platforms in the market. Fixed-wing aircraft also provide global connectivity, enabling efficient and rapid transportation between distant locations. As globalization expands, the demand for fixed-wing aircraft and aerostructures to support international travel and trade remains strong.

The material segment includes alloys & superalloys, composites and metals. The alloys & superalloys segment dominated the market, with a share of around 44.37% in 2022. Alloys and superalloys are known for their excellent strength-to-weight ratio. In the aerospace industry, where minimizing weight is necessary for fuel efficiency and overall performance, these materials are favoured for their ability to provide high strength while keeping the weight of aerostructures relatively low. Superalloys are designed to withstand high temperatures, making them suitable for components exposed to extreme conditions, such as jet engines and exhaust systems. Their ability to maintain mechanical properties at elevated temperatures contributes to their aerostructure dominance. In addition, alloys and superalloys exhibit exceptional durability and resistance to fatigue, making them well-suited for the demanding conditions experienced by aircraft components. The ability to withstand cyclic loading and stress is critical for aerostructures' structural integrity and safety.

The end user segment is split into OEM and aftermarket. The aftermarket segment dominated the market, with a share of around 62.13% in 2022. The aftermarket is crucial for providing ongoing maintenance, repair, and overhaul services to ensure the continued airworthiness of aircraft. Aerostructures, integral parts of an aircraft, require regular inspections, repairs, and replacements throughout their operational life. Further, the aftermarket becomes increasingly important as aircraft age and continue in service beyond their initial design life. Upkeep of aerostructures becomes essential to extend the service life of ageing fleets, contributing to the aftermarket's significance. Most importantly, aircraft operators often invest in aftermarket services to incorporate upgrades, modifications, or retrofitting of aerostructures. This aspect allows for integrating new technologies, enhanced performance features, and compliance with evolving regulatory standards.

| Attribute | Description |

|---|---|

| Market Size | Revenue (USD Billion) |

| Market size value in 2022 | USD 62.28 Billion |

| Market size value in 2032 | USD 118.23 Billion |

| CAGR (2023 to 2032) | 6.62% |

| Historical data | 2019-2021 |

| Base Year | 2022 |

| Forecast | 2023-2032 |

| Region | The regions analyzed for the market are Asia Pacific, Europe, South America, North America, and Middle East & Africa. Furthermore, the regions are further analyzed at the country level. |

| Segments | Components, Aircraft Type, Material, and End User |

As per The Brainy Insights, the size of the aerostructures market was valued at USD 62.28 billion in 2022 to USD 118.23 billion by 2032.

The global aerostructures market is growing at a CAGR of 6.62% during the forecast period 2023-2032.

North America became the largest market for aerostructures.

Rising demand for commercial aircraft and advancements in material technologies drive the market's growth.

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. The Brainy Insights has segmented the global Aerostructures market based on below-mentioned segments:

Global Aerostructures Market by Components:

Global Aerostructures Market by Aircraft Type:

Global Aerostructures Market by Material:

Global Aerostructures Market by End User:

Global Aerostructures Market by Region:

Research has its special purpose to undertake marketing efficiently. In this competitive scenario, businesses need information across all industry verticals; the information about customer wants, market demand, competition, industry trends, distribution channels etc. This information needs to be updated regularly because businesses operate in a dynamic environment. Our organization, The Brainy Insights incorporates scientific and systematic research procedures in order to get proper market insights and industry analysis for overall business success. The analysis consists of studying the market from a miniscule level wherein we implement statistical tools which helps us in examining the data with accuracy and precision.

Our research reports feature both; quantitative and qualitative aspects for any market. Qualitative information for any market research process are fundamental because they reveal the customer needs and wants, usage and consumption for any product/service related to a specific industry. This in turn aids the marketers/investors in knowing certain perceptions of the customers. Qualitative research can enlighten about the different product concepts and designs along with unique service offering that in turn, helps define marketing problems and generate opportunities. On the other hand, quantitative research engages with the data collection process through interviews, e-mail interactions, surveys and pilot studies. Quantitative aspects for the market research are useful to validate the hypotheses generated during qualitative research method, explore empirical patterns in the data with the help of statistical tools, and finally make the market estimations.

The Brainy Insights offers comprehensive research and analysis, based on a wide assortment of factual insights gained through interviews with CXOs and global experts and secondary data from reliable sources. Our analysts and industry specialist assume vital roles in building up statistical tools and analysis models, which are used to analyse the data and arrive at accurate insights with exceedingly informative research discoveries. The data provided by our organization have proven precious to a diverse range of companies, facilitating them to address issues such as determining which products/services are the most appealing, whether or not customers use the product in the manner anticipated, the purchasing intentions of the market and many others.

Our research methodology encompasses an idyllic combination of primary and secondary initiatives. Key phases involved in this process are listed below:

The phase involves the gathering and collecting of market data and its related information with the help of different sources & research procedures.

The data procurement stage involves in data gathering and collecting through various data sources.

This stage involves in extensive research. These data sources includes:

Purchased Database: Purchased databases play a crucial role in estimating the market sizes irrespective of the domain. Our purchased database includes:

Primary Research: The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. Primary research mainly involves in telephonic interviews, E-mail interactions and face-to-face interviews with the raw material providers, manufacturers/producers, distributors, & independent consultants. The interviews that we conduct provides valuable data on market size and industry growth trends prevailing in the market. Our organization also conducts surveys with the various industry experts in order to gain overall insights of the industry/market. For instance, in healthcare industry we conduct surveys with the pharmacists, doctors, surgeons and nurses in order to gain insights and key information of a medical product/device/equipment which the customers are going to usage. Surveys are conducted in the form of questionnaire designed by our own analyst team. Surveys plays an important role in primary research because surveys helps us to identify the key target audiences of the market. Additionally, surveys helps to identify the key target audience engaged with the market. Our survey team conducts the survey by targeting the key audience, thus gaining insights from them. Based on the perspectives of the customers, this information is utilized to formulate market strategies. Moreover, market surveys helps us to understand the current competitive situation of the industry. To be precise, our survey process typically involve with the 360 analysis of the market. This analytical process begins by identifying the prospective customers for a product or service related to the market/industry to obtain data on how a product/service could fit into customers’ lives.

Secondary Research: The secondary data sources includes information published by the on-profit organizations such as World bank, WHO, company fillings, investor presentations, annual reports, national government documents, statistical databases, blogs, articles, white papers and others. From the annual report, we analyse a company’s revenue to understand the key segment and market share of that organization in a particular region. We analyse the company websites and adopt the product mapping technique which is important for deriving the segment revenue. In the product mapping method, we select and categorize the products offered by the companies catering to domain specific market, deduce the product revenue for each of the companies so as to get overall estimation of the market size. We also source data and analyses trends based on information received from supply side and demand side intermediaries in the value chain. The supply side denotes the data gathered from supplier, distributor, wholesaler and the demand side illustrates the data gathered from the end customers for respective market domain.

The supply side for a domain specific market is analysed by:

The demand side for the market is estimated through:

In-house Library: Apart from these third-party sources, we have our in-house library of qualitative and quantitative information. Our in-house database includes market data for various industry and domains. These data are updated on regular basis as per the changing market scenario. Our library includes, historic databases, internal audit reports and archives.

Sometimes there are instances where there is no metadata or raw data available for any domain specific market. For those cases, we use our expertise to forecast and estimate the market size in order to generate comprehensive data sets. Our analyst team adopt a robust research technique in order to produce the estimates:

Data Synthesis: This stage involves the analysis & mapping of all the information obtained from the previous step. It also involves in scrutinizing the data for any discrepancy observed while data gathering related to the market. The data is collected with consideration to the heterogeneity of sources. Robust scientific techniques are in place for synthesizing disparate data sets and provide the essential contextual information that can orient market strategies. The Brainy Insights has extensive experience in data synthesis where the data passes through various stages:

Market Deduction & Formulation: The final stage comprises of assigning data points at appropriate market spaces so as to deduce feasible conclusions. Analyst perspective & subject matter expert based holistic form of market sizing coupled with industry analysis also plays a crucial role in this stage.

This stage involves in finalization of the market size and numbers that we have collected from data integration step. With data interpolation, it is made sure that there is no gap in the market data. Successful trend analysis is done by our analysts using extrapolation techniques, which provide the best possible forecasts for the market.

Data Validation & Market Feedback: Validation is the most important step in the process. Validation & re-validation via an intricately designed process helps us finalize data-points to be used for final calculations.

The Brainy Insights interacts with leading companies and experts of the concerned domain to develop the analyst team’s market understanding and expertise. It improves and substantiates every single data presented in the market reports. The data validation interview and discussion panels are typically composed of the most experienced industry members. The participants include, however, are not limited to:

Moreover, we always validate our data and findings through primary respondents from all the major regions we are working on.

Free Customization

Fortune 500 Clients

Free Yearly Update On Purchase Of Multi/Corporate License

Companies Served Till Date